2021 is Different Than 2007

Six reasons why the real estate boom has legs to run

When I was an investment advisor, it always seemed like the shadow of the 1929 stock market crash and its subsequent aftermath loomed large in all sorts of conversations I would have with clients who were planning for retirement, saving for their kids’ college education, or just trying to build up a nest egg. The experience of the Great Depression is burned into the collective memory of our country whether a person lived through it or not. Everyone believes that fortunes can be lost seemingly overnight and that once things get too hot they are supposed to inevitably drop.

The Great Recession of 2008-2009 is something most of us did actually live through and is a more recent example that things can go south in a hurry. The collective wisdom holds that a housing bubble was the culprit for this economic downturn as banks had offered too many home loans to people who should not have qualified and then consumers with subpar credit were suddenly not able to afford their mortgage payments when variable rates kicked in. The impact from mortgage defaults rippled through the economy because all of these sub-prime mortgages had been collateralized into new investments by banks and when the mortgages blew up, so too did all the investments.

As recently as last week’s column I urged caution in the face of what by all accounts is a strange economy. I take Warren Buffett’s sage investment advice to heart when he says, “Be fearful when others are greedy and be greedy when others are fearful.” And there is certainly a lot of greed out there right now.

But I also spend a considerable amount of my time as a banker analyzing the housing market and real estate in general. And I think that despite wild stories of how inflated prices have become, the housing market is actually not in a bubble and has room to run. Ideally prices would level out a bit and give potential homebuyers a breath so they can find homes within their desired price range. That kind of a graceful leveling off might be optimistic. But I do not share the pessimism that just because the housing market has been so good for the past several years (and especially since the outset of COVID-19) that it must inevitably drop.

It is also worth noting that a leveling off of prices, which, again, would be nice in many ways at least on the buyer’s side of the equation, does not necessarily constitute a bubble popping or serve as a catalyst for some kind of major reversal in the housing market and subsequent economic downturn.

Here are the reasons why I think the housing market is, in fact, in a mostly rational place despite the wild run-up in prices over the last year and a half.

#1: Interest rates are being kept low

Concerns about what is perceived as a structurally weak economy with unemployment rates that are still too high have led the Fed to commit to keeping interest rates low until 2023. When interest rates are low, people are more willing and able to take on new debt including mortgages. And you can buy more house at a 3.00% interest rate than, say, a 5.00% interest rate. Until interest rates rise in any sort of meaningful way, the strength of the housing market will continue.

#2: Homebuyers are more stable today than in 2007

Thanks in part to tightened credit standards that were established following the 2008 financial crisis and thanks in part to a recovering economy and COVID-related stimulus programs, consumers are in a stronger place today than they were in 2007. The median credit score for a new homebuyer in the first three months of 2021 was a whopping 788; by comparison, the average credit score for a new homebuyer in the first quarter of 2007 was 712. The stronger creditworthiness among borrowers should lead to fewer defaults and less general disruption in the housing market. Curiously enough, as illustrated in the chart below, credit scores have actually improved during COVID as people have taken discretionary income they might have otherwise spent on travel and entertainment and paid off debt instead. Multiple rounds of stimulus have also helped significantly.

Homeowners also have better balance sheets today than in 2007. As a pair of tweets and charts from housing analyst Odeta Kushi show, homeowners currently have a record amount of equity in their homes, plus savings and personal incomes are at strong levels (although spending has ramped up a bit in recent months as people are proceeding with less caution thanks in large part to vaccines).

I spoke with realtor Aaron Chadbourne this week, who noted the fact that many homebuyers are coming to the market from a position of greater strength today versus 2007. He told me, “A big difference between now and then is the amount of cash people are using for down payments. Back then people were getting 100% financing and sometimes more. Now people are flush with cash. With large down payments they have immediate built-in equity.”

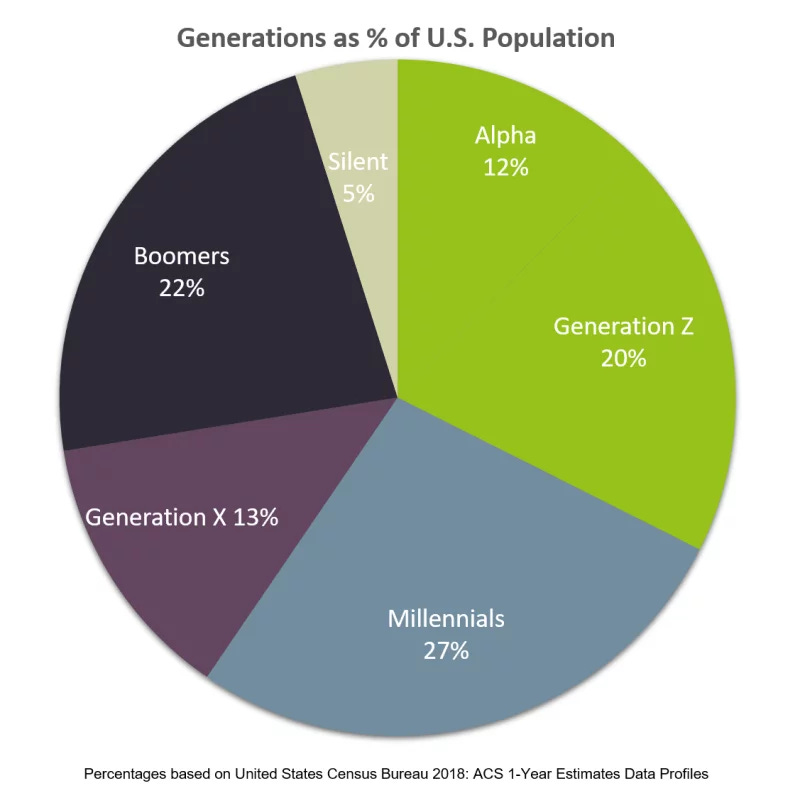

#3: A generation of home-buyers is coming of age

Millenials and Gen Z now make up 47% of the population. Both generations have been less likely to buy homes than members of previous generations, but that is shifting as young people come of age and build up the savings and creditworthiness necessary to buy a home. According to Realtor.com, 4.7 million people turned 30 last year, which is the start of one’s peak home-buying years. There are a lot of Americans age 18-40 who have never owned a home before who are now potential buyers, which could put wind in the sails of the housing market for quite some time.

#4: The rents are too damn high

The cost to rent continues to climb, up 11.4% nationwide since January and even more in certain pockets of the country. There seems to be no sign of this slowing. As renting becomes more expensive, people will look to buy homes instead (the Substitution Effect in practice, to use an economics term). Aaron Chadbourne also noted to me that a lot of younger people have been living at home with their parents post-college to save money and have continued to do so during COVID. Now they want out and they don’t like the look of the rental market very much, so they are more commonly looking to buy. As Taylor Marr, lead economist at Redfin notes:

#5: Supply chain issues will settle out

Part of the reason the housing market may feel overheated is that there has been less inventory on the market, which has driven prices up. When supply is low but demand is high, prices will rise, and rise they have to almost feverish levels. The housing market is littered with stories of homes selling way over list price and buyers doing crazy things like paying competing buyers to walk away or offering to name their children after sellers. But the underlying variable here is that demand is just so strong for homes. Given the limited inventory, of course prices are going to rise. But that does not necessarily constitute something irrational that would suggest a bubble (although reasonable people can debate on whether offering to name your child after a seller is rational or not).

Once supply chain issues settle out and the prices of materials subside, homebuilders will have fewer challenges building new homes and they will be able to do so for lower prices, which will create additional inventory of homes for sale. This could have the positive effect of both leading to more homes being purchased and an easing of prices as supply increases to match demand.

There is already evidence that COVID-related supply chain issues are, in fact, easing. Lumber futures have cratered over the past three months, for example. Although as economic Ali Wolf notes, significant supply chain issues do remain and sometimes for the most random of items:

#6: Institutional buyers provide a base of demand for homes

I want to offer a caveat on this point that I do not necessarily think what I am about to point out here is a good thing, certainly not if you’re addressing the buyer’s side of the equation: the housing boom is also being driven by institutional buyers scooping up as many homes as they can. Ryan Dezember has an article in the Wall Street Journal about a company called Tricon Residential that is planning to buy 18,000 rental properties as a source of investment income for a Texas pension fund. Another huge investment company, BlackRock, also appears to be buying up homes around the country. Elena Botella from Slate notes that companies like BlackRock purchased 15% of all U.S. homes for sale in the first quarter of 2021.

This is clearly not good news for buyers looking to acquire their own personal residence. It is hard to compete with an investment company that is looking only in terms of potential cash flow from renting out homes and can afford to pay significantly over asking price and without needing bank financing. Sellers may want to pass their home along to the proverbial nice-young-family who are just getting started out, but when a cash offer from an institutional buyer $50,000-$100,000 over asking price comes in, what are most sellers going to do?

There is a case to be made that the robust home market is severely detrimental to first-time homebuyers and buyers in the low to moderate price range. Ali Wolf, whom I referenced above with the tweet above about supply chain issues, recently had a thought-provoking piece in the New York Times about who is getting left out in the current housing market, noting:

This is not an equal-opportunity boom. The housing rebound has been fueled by buyers whose wealth allowed them to win bidding wars, often with a high down payment and a bid over asking price. Those living on local incomes, which are often modest compared with those of relocating newcomers, are losing the ability to buy a home as competition grows and prices rise. In the long run, this means some Americans will be able to build wealth in their homes, leaving the rest behind.

Institutional buyers purchasing up tens of thousands of homes across the country certainly does not help this equation.

Bonus Reason #7 - Certain markets will do better than others

I was watching the news earlier this week and the stories about severe drought and wildfires in California made me wonder whether there will be climate-related migrations of people within this country in the years to come. You can make a case that this has already started. Last year California’s population declined for the first time since 1850. There are certainly other reasons for this besides droughts and fires, but those are a part of it. Certain areas of the country will benefit from this, like Maine where I live. Couple climate migrations with a paradigm shift in the way we work as more and more companies are offering and even encouraging remote options, and the implications for local housing markets around the country are profound.

To conclude here, the housing market has been crazy for the past year, there is no doubt about that. The CEO of Redfin had a 15-point Tweetstorm summarizing some of the wildest stories in real estate over the past few months. I’d encourage people to read the thread both for the perspective and entertainment value.

But it is important to remember there is a difference between a strong market and a bubble. Just because prices are rising doesn’t mean there is a bubble that is about to imminently pop, nor does a possible drop or leveling off of home prices represent a popping of a bubble. In my opinion the market might ease (in a good way) over the next 12 months as consumers pull back and wait out the rapidly rising prices. A pull-back like this should be interpreted as a positive thing because it shows some rationality. Lower lumber prices will help too as homebuilders will be able to buy more homes for less as material prices come down.

Thank you to everyone who is already a subscriber to The Sunday Morning Post newsletter. If you’re not a subscriber yet just click below and you’ll get researched analysis like this (for free) in your inbox each Sunday morning. Thanks for reading.

Ben Sprague lives and works in Bangor, Maine as a V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram and subscribe to this weekly newsletter by clicking above.

Author’s Note

Thank you to everyone who read and shared my article last week, “The Eat-Drink-And-Be-Merry-For-Tomorrow-We-Die Economy.” It was one of my most-read articles yet and I appreciate the words of support and shares.

A lot of you seem to enjoy the Weekly Round-up of links at the end of these articles each week. I spent a good portion of the past week offline, so check back next week for extra links! For now, here is a summertime Olympic spread from Newcenter Meteorologist Jessica Conley:

Have a great week, everybody!