A Home as an Inflation Hedge

On a conference call with investors this past week, the Executive Chairman of Lennar Corporation, which is a Florida-based homebuilder, offered comments that linked two of the hottest issues in the economy: housing and inflation. He said:

Buyers are seeking shelter and they are seeking shelter from inflationary pressures as scarce rentals see rents escalating and escalating housing costs can be controlled with an owned home with a fixed-rate mortgage, while wages are going up, so too our housing costs. So with employment strong and home prices rising, it is best to fix these costs.

Additionally, the home is ever more the control center or hub of our customers' lives and frankly, geopolitical stress makes the security of home all that much more comforting. While demand is strong, supply is short and constrained, the ability to actually build and deliver homes has been slowed by the supply chain that is all but broken, by the workforce that is short in supply, and the intense competition for scarce and titled land assets. Therefore, the supply of homes has remained quite limited and is not prone to overbuilding.

The Chairman, Stuart Miller, offered upbeat guidance on expected home sales for the rest of the year and expressed optimism even amid rising interest rates and other challenges in the global economy. Lennar stock rose almost 10% this week amid a broader market rally.

Shelter from Inflation

Demand for new homes has risen over the past year for all kinds of reasons. A generation of new homebuyers is coming of age, interest rates have been at historically low levels, and the pandemic sparked inward-looking behavior from American consumers, suddenly much more mindful of the comfort and quality of their own homes. One factor I had not considered until reading the comments from the Lennar Executive Chair, however, is inflation.

Prices have soared in virtually all types of goods and services over the past year:

Gas: +38%

New vehicles: +12% (used vehicles: +45%!!)

Electricity: +9%

Food: +8%

Transportation: +7%

Apparel: +6%

Rent inflation, which normally runs on an average of 3-4% per year, was 11% in 2021. Rents for single-family homes were up a staggering 26% in 2021. It makes sense that amid the uncertainty that comes with all these rising pries people would be looking to control one of them, and one way to do that is to fix housing costs at a set payment for the life of a traditional 30-year mortgage.

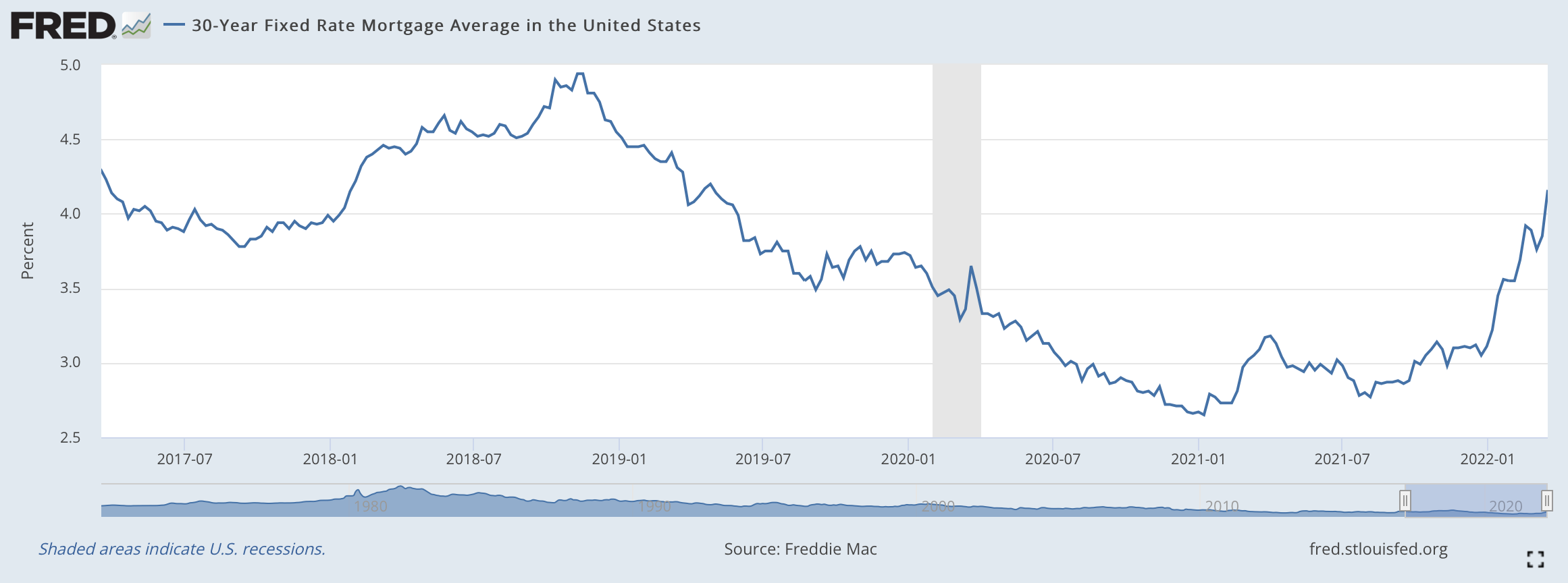

One of the key questions for the U.S. housing market right now is whether sharply rising interest rates will put a damper on rapidly rising prices. The chart below shows the average rate on a 30-year fixed rate mortgage in the United States over the last five years. The increase in recent weeks is evident. In fact, the average nationwide rate on 30-year mortgage has increased from 3.11% during the last week of 2021 to 4.16% today, a mere eleven weeks later.

Conventional wisdom is that rising rates will cool the housing market. In conversations with my colleagues who do residential loans, however, loan applications have not slowed down. Applications for refinances have dropped off a cliff, but new home loan applications remain brisk. Applications for new home construction are particularly strong, no doubt fueled by the very low inventory on the market of existing available homes; if prospective homebuyers can’t find a house to buy, they are instead looking to build one. In fact, new housing starts were up 6.8% in February.

If interest rates continue to dramatically spike and the average 30-year fixed rate soars to, say 6.00%, it will have an impact. In the meantime, however, given just how much demand there is among potential homebuyers, the housing market should have room to run on even as rates do begin to rise. And if inflation remains high particularly with regard to rental inflation, there is reason to believe that buyers will remain as motivated as ever.

Ben Sprague lives and works in Bangor, Maine as a V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram and subscribe to this weekly newsletter by clicking below.

Weekly Round-Up

Here are three things that caught my eye around the web this week:

There are 1.5 million real estate agents in the United States and only 376,000 homes to sell. “This is a savagely unhealthy housing market,” one real estate agent says. Read more via Business Insider.

The average homeowner is staying in their home 13.2 years, up from an average of 10.1 years a decade ago. Read more via RedFin.

There is correlation between rising interest rates and economic recessions. Via the Calculated Risk blog, “Most of the post-WWII recessions were caused by the Fed tightening monetary policy to slow inflation…Usually, when inflation starts to become a concern, the Fed tries to engineer a ‘soft landing’, and frequently the result is a recession.” Read more.

On a more positive note, gas prices inched down this past week from an average of $4.326 to an average of $4.262. While that is not a huge drop, the rocketing up of prices over the last month at least leveled off and, in fact, modestly reversed. Here in Maine, the average price dropped from $4.274 to $4.197 over the past seven days. Read more.

Have a great week, everybody!