A Noisy Week of Housing Data

Plus: what is going on with the price of eggs?

Like two rivers swirling together in a churning vortex, so too did push-and-pull forces of supply and demand collide this week in a real estate market struggling for direction. Let’s dig into some numbers from a noisy week of data:

Interest Rates

After peaking above 7.00% in early November, the rate on a conventional 30-year fixed residential mortgage dropped all the way to 6.15% this week. The chart below shows the average 30-year fixed rate over the last five years. Evident is the big run-up over the last year, but also the downward movement over the past few weeks:

Just as a side note here, residential and commercial rates have diverged a bit in the last few months. Whereas residential rates have edged down, commercial rates remain high at least relative to the previous few years. At least for the bank where I work, commercial rates are typically priced at a margin above Prime Rate. Prime Rate from March 2020 to March 2022 sat at 3.25%. It has now been hiked by the Federal Reserve all the way to 7.50% with expected increases to 7.75% and 8.00% (or more) over the next couple of months. It may be another 10-12 months or longer before there is any meaningful reduction in commercial interest rates. So while residential rates have eased down in the last few weeks, commercial rates remain high.

Mortgage Applications

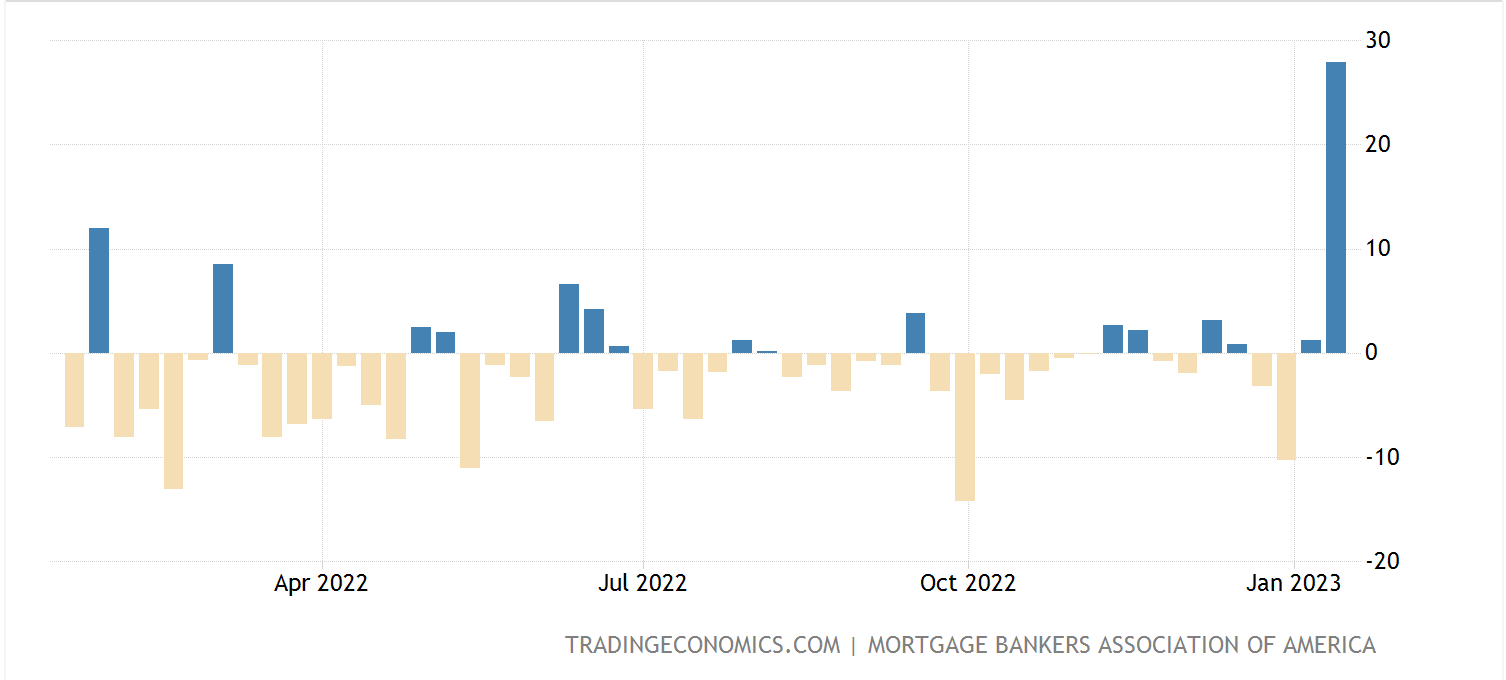

Mortgage applications somewhat unexpectedly surged by 27.9% last week, which shows how sensitive buyers are to lower rates. With rates being down at the moment, mortgage applications are way up according to the Mortgage Bankers Association. In fact, the 27.9% weekly increase was the largest jump since March 2020 and one of the biggest jumps in the last ten years. Some of this may be seasonal as people have made it through the holidays and are starting fresh in the new year, but I really do think the driving variable is the lower interest rates.

Applications for mortgage refinances were also up significantly last week, increasing by 34.2%, which is most likely a sign of recent buyers trying to capture the benefits of lower rates almost immediately after closing on their original loans in recent months. It may cost borrowers the extra closing costs of doing a refinance, but saving half a percentage point or more can make a difference of tens of thousands of dollars over the life of a mortgage.

The chart below shows relative weekly changes in mortgage applications over the last year. There are a lot of weekly declines (yellow lines) as compared to increases (blue lines). This past week is clearly an outlier and may signal buyers coming back to the market at least for the time being, although perhaps also the seasonality mentioned above with the start of a new year:

Homebuilder sentiment

After a year of steadily declining sentiment from homebuilders, the index ticked up this month for the first time since December 2021. Why? From some of the homebuilders I have spoken to recently, their moods have been buoyed of late by several variables. Building material costs are down. Labor markets, although still tight, are loosening slightly and contractors and subs are more readily available. And, most importantly, it is the interest rates being down for buyers. Lower rates (at least relative to a couple of months ago) give homebuyers more purchasing power, not to mention keeping them in a buying mood in general.

The chart below shows homebuyer sentiment over the last 12 months (don’t worry so much about what the number above each column means; it is based on a complex formula and calculation. The important thing is just the relative changes. The higher the number, the more confident homebuilders are feeling). You can see after steady declines over the last year, there was an uptick this month. Although sentiment is still decidedly negative, the bottoming out and slight rebound is notable:

New Housing Starts

Data released on Thursday by the U.S. Census Bureau and HUD presents a mixed picture on new housing starts. On the one hand, single-family housing starts ticked up in December to a seasonally adjusted number of 909,000 homes versus a rate of 817,000 homes in November. However, these 909,000 homes were down from a rate of 1,212,000 homes one year prior in December 2021.

Is this slight uptick a sign of a market that is finding a floor? Possibly, as long as mortgage rates stay in the low 6.00% range and the economy holds up (i.e. people keep working, earning money, and feeling economically secure).

The new housing starts are also likely a symptom of a lack of existing inventory on the market. Although the home market has slowed considerably, there is still very little inventory for sale, which means people are building new homes instead for a lack of other options.

On the multifamily side of things, multifamily construction (defined as properties with 5+ units) dropped from a seasonally-adjusted rate of 571,000 in November to 463,000 in December. The 463,000 figure in December 2022 is also down 16.3% from the 533,000 multifamily starts one year prior in December 2021. My suspicion is that the higher commercial rates, which impact many builders, are cooling off the market for that type of construction in a way that is different from single-family home construction, for which interest rates have generally dropped in the past two months. Builders, too, are rate sensitive as the margins for projects just do not work as well when you are borrowing at a high interest rate. For a sustained increase in multifamily construction, commercial interest rates will need to come down from their current levels.

Inflation

Inflation continued decelerate in December, with prices increasing on an annual basis by 6.5%. Gas and energy prices were down 4.5%, providing some relief to the many Americans struggling with these high costs. Food prices and shelter costs (homes and rent) continued to rise, although as I’ve discussed before much of the data for shelter lags by several months and there is ample evidence that both home prices and rents are stabilizing and even starting to decline. I expect inflation will continue to drop in the months ahead. This will provide some impetus to the Federal Reserve to stop hiking interest rates so much, which would be good for the overall housing and construction markets. Nevertheless, the Fed has been very hawkish on inflation and quarter-point interest rate hikes are still expected at least once or twice in the several months ahead.

Eggs

Finally, on a completely separate note, what is going on with the price of eggs? The average price for a dozen was about $1.93 one year ago. Now it is all the way up to $4.25. According to the U.S. Department of Agriculture, egg prices were up 59% in December alone. This is really challenging for consumers at the grocery store, but also for restaurants that use a lot of eggs as ingredients.

The primary reason for the increase? While there are some supply chain issues out there, the driving factor is the avian flu. As consumers pull back from eggs in the face of these high prices and as, hopefully, the avian flu declines, egg prices should return to more of an equilibrium. The chart below shows the major run-up over the last year.

To Sum It Up

So to sum up a busy week of data:

Home loan interest rates are down (although commercial rates remain up)

Mortgage applications are up

Homebuilder sentiment is still pretty negative, but improved this month for the first time in a year

Single-family home construction is up

Multi-family construction is down

Inflation, though still high, is on its way down

Egg prices are crackingly high

What I am looking at in the week ahead? On Thursday we will see some fresh data on new home sales, which I expect to be down. And on Friday we will see some numbers from the University of Michigan consumer sentiment survey for the month of December. I expect sentiment will have improved slightly thanks for lower gas prices, although this will be tempered by high prices on other things including food.

Have a great week, everybody.

Ben Sprague lives and works in Bangor, Maine as a Senior Vice President/Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram. Opinions and analysis do not represent First National Bank. © Ben Sprague 2023.

Huh. My favorite brand of organic eggs disappeared for about 6-8 weeks and then reappeared - but I hadn't noticed much higher prices, because I was already buying the high end segment (better eggs). Gas prices bottomed at 2.79ish (I saw 2.74) and then rebounded a bit to 3.09-3.19, although I saw a couple of 3.29s and a 3.39 at a rural speedway on the interstate. Diesel prices remain locked in at a dollar higher than ethanol gas prices, which is strange - I remember the 80's and 90's and diesel prices remained higher gas but stable - not anymore - although the differential over a year ago has dropped.

Back before Thanksgiving, the local Scouts did their annual pickup food drive collection (I do give money to the foodbank - but these are kids trying to do their bit), so I picked up various (new, not expired!) staple goods at the store for them. Rice, dried beans, canned tomatoes, Uncle Ben's, dehydrated potatoes, a six-pack of ramen in a cup, that kind of thing - all those prices were in the reasonable range, maybe .10-.20 cents higher at most.

I watch beef prices pretty closely - the Walmart steak price is 10.97$/lb, which is 1$ higher than the per pound price in January 2019. A big piece of chuck roast is 5.47$ - which is pretty close to where it was circa January 2019. Overall, those kinds of prices are roughly 10-15% or less higher than where they were four years ago. Veggies are currently suffering their seasonal scarcity, but bell peppers are 1.25$ each, which is about the high price I see every winter, for years now. If there's a difference, it's a mild decline in quality and availability. (Parsley quality is terrible every winter but it's abysmal this year. As are the cucumbers - carrots and potatoes are ok.)

Snack foods - are ridiculous. I pick up the family-sized m&m's for my elderly step-father every week: a year ago 8.92 would've been the price at Walmart, 10.97 the price at the Martin's/Giant. A month ago it was 10.94 and 12.97, just after new year's it was 12.94 and 15.98. I see the same pattern in soft drinks, cookies, not quite so much in the breakfast isle. It seems that segment of manufacturers are leaning hard into gouging to boost profits ahead of an anticipated recession.

Overall, I don't see anything to warrant the flipping out about inflation I've been seeing from the usual suspects for the last two years. It reads to me that we took a one-time 10% increase in the base price level over four years (oil excluded), with some anticipatory profiteering to offset potential wage increases.

elm

so