An Early Look at Rising Rates

Refinance requests have already plummeted 54%

Author’s Note: I frequently speak to groups and organizations about the economy, real estate, and housing. If your group is interesting in me presenting, please email me at ben.sprague@thefirst.com or bsprague1@gmail.com. I am available in-person depending on the geographic logistics or via Zoom.

An Early Look at Rising Rates

Two weeks ago I wrote about how you can draw a straight line from January’s strong jobs report to interest rate hikes this coming March. I won’t dwell on the reasons why today other than to link to that previous article in case you want to read or review it.

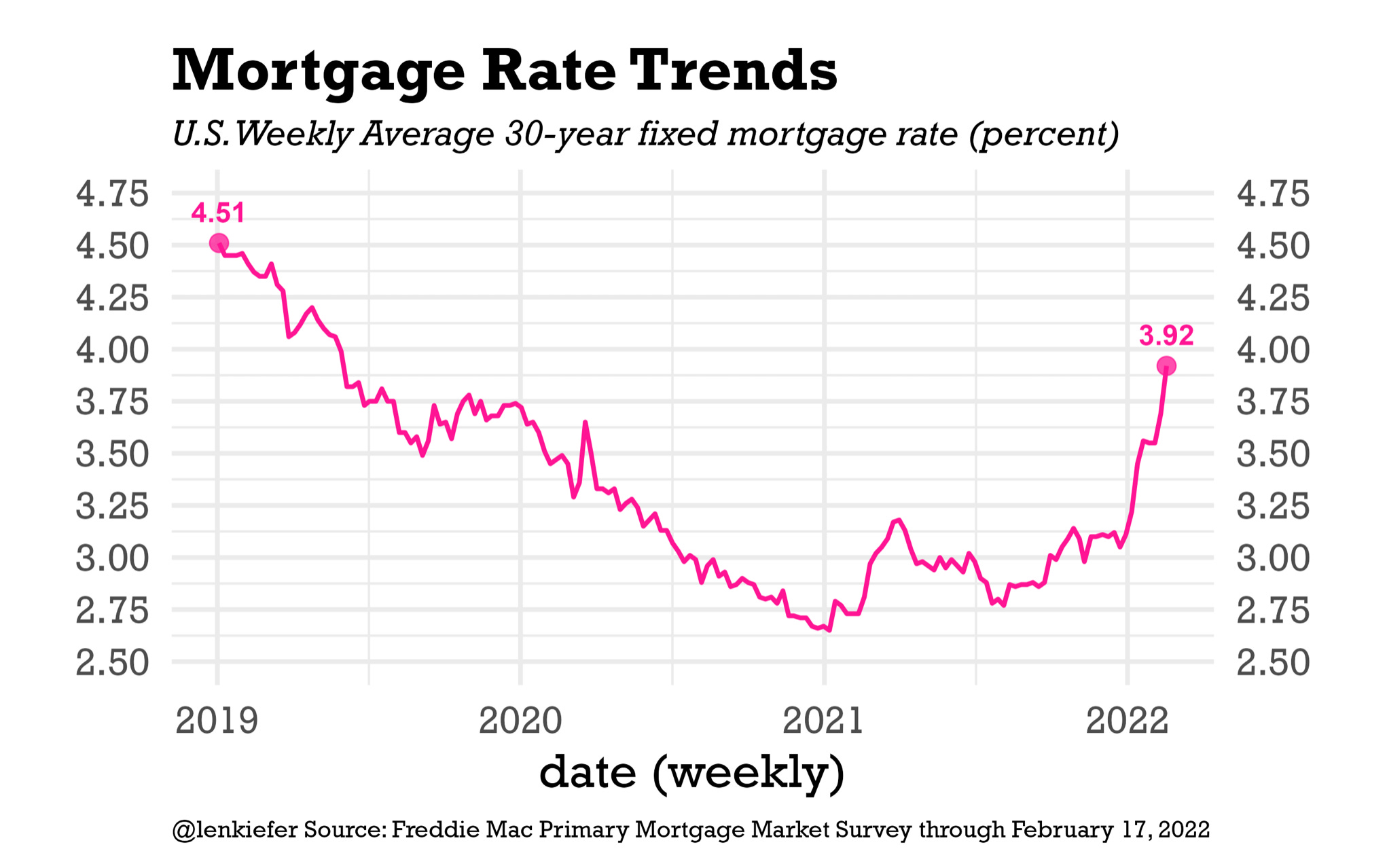

What has been surprising even to me is that these expected rate increases are rapidly getting baked into bank loans around the country. Consider this chart from Len Kiefer, Deputy Chief Economist at Freddie Mac, which shows the average rate on a 30-year fixed mortgage:

The average rate is quickly approaching 4.00% having been just over 3.00% at the start of the year. There are two immediate implications for homebuyers and homeowners:

The cost of borrowing is increasing, adding yet more frustrations to an extremely challenging housing market for homebuyers especially first-time homebuyers.

The opportunity to refinance existing mortgages has passed for many. Mortgage analytics company Black Knight reported this week that 3.8 million American homebuyers could still benefit from a refinance, which on the surface seems like a lot of people, but that figure is down from 5.1 million Americans just one week prior and down from 11 million at the start of the year. The window is closing for people who want to refinance. In fact, according to the Mortgage Bankers Association, applications for refinances this past week were 54% lower than this same week one year ago (which also reflects the fact that so many people can and did refinance over the past 12-24 months; there just aren’t that many people left who still want to and can).

Impact on the Housing Market

There are some who believe that the anticipation of rising rates is going to lead to a flood of new mortgage applications and that we may see an extra bump up in both prices and transactions over the next few months as prospective homebuyers rush to lock in low rates. I am sure there will be some who will accelerate their plans, but my perspective on the current housing market is that demand is already so strong that there are few catalysts that are likely to make buyers even more hot to trot. In other words, people who want to buy have been eager to do so for months now; the rise in interest rates is not going to motivate people any further who are already quite highly motivated to begin with.

In the intermediate to longer term, higher rates will have a dampening effect on the housing market. People will not be able to take on as large of loans, which will act as a bit of a weight on prices throughout the price spectrum. Bank underwriters will have to include higher monthly payments on proposed loans in their calculations and some applicants will no longer quality, which will remove a portion of the prospective buyer pool, further dampening the market.

What the Fed will hope to do by raising rates is achieve a Goldilocks version of economic growth: not too hot and not too cold. That is a tough needle to thread, although there are plenty of reasons to argue that the housing market will actually hold up even amid rising rates. These reasons include the fact that homebuyer demand is just so strong right now, there are millions of prospective homebuyers among the Millennial and Gen Z generations coming of age, and despite serious and well-founded concerns about inflation, the state of the American consumer is actually fairly strong in aggregate.

What I’m Seeing

In my work as a commercial lender for First National Bank here in Maine, I have not yet seen much of a slowdown in new loan requests compared to, say, a month ago, six months ago, or a year ago. Interest rates have started to rise in the commercial lending world too, but as of now we remain extremely busy with all types of commercial requests.

In speaking to my colleagues on the residential side, they have seen a slowdown in refinance activity, which mirrors the national trend as noted above. The volume of home loan requests for acquisition or construction remains brisk but manageable.

What will be interesting to see, of course, is what happens if the 30-year fixed rate continues its rapid rise from around 4.00% to, say, 5.00% or even more. This is only a gut-level feel, but I suspect if the average 30-year fixed rate leaps too much above the mid-4.00’s and touches 5.00% or more, the Goldilocks equation will quickly start trending towards too cold at least in terms of the housing market, although depending on your perspective that may be a good thing. Plenty of prospective buyers might trade higher payments due to greater interest rates for a dampening of prices and a less competitive buyers’ market. Stay tuned.

Ben Sprague lives and works in Bangor, Maine as a V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram.

Weekly Round-Up

Here are five things that caught my eye this week that I wanted to share with you.

It is a principal of economics that inefficient markets correct themselves. Right now there is an undersupply of homes. Inventory is seriously low and demand among homebuyers is high. But, we are also now building new homes at a more rapid pace than at any point since 1973. The market is correcting, although it may take years for us to reach equilibrium.

Two MIT professors shared a study last month showing that mindfulness apps actually seem to work. Participants reported less stress and anxiety than those in a control group and showed improved decision-making and work skills.

Even Disney is getting into the residential housing market. Per USA Today, “The first community, which will be known as Cotino, will include about 1,900 housing units and will be in the Palm Springs city of Rancho Mirage, California.” On an semi-related note, Disney just reported blockbuster earnings, beating estimates on both revenue and EPS:

Disney delivered revenue of $21.8 billion in its fiscal first quarter ended Jan. 1 when Wall Street analysts expected $18.6 billion. Similarly, Disney reported earnings per share of $1.06 in Q1 when Wall Street expectations were $0.61.

Per Rental Property Analyst Jay Parsons, rental occupancy right now is a staggeringly high 97.6%. When underwriting rental property deals for borrowers/buyers, most banks (including mine) assume vacancy rates of 10% for the sake of conservative analysis. Why is occupancy so high? That’s a good question for a future newsletter.

Have a great week, everybody! To reach me personally of professionally, please email me at bsprague1@gmail.com or ben.sprague@thefirst.com.

Very interesting article Ben. My take on this is the housing market might be able to ride through 4 or 5% percent. We've got a lot of people who have opted out of buying a home the last two years due to covid and instead opted to keep saving until it is safe to shop around. That's 24 extra months of saving (not to mention the stim checks). With the rise of vaccinated people versus non- vaccinated and covid restrictions slowly being lifted; I have a feeling the housing market will be fueled by the people who have been saving and waiting and now have the money for a 1-2% change in the market.