Are We in a "New Housing Crisis?"

Digesting a Claim from the National Association of Realtors

Nearly five years ago, I wrote an article entitled, “2021 is Different than 2027.” I was writing in response to concerns that the housing market was getting overheated. There is sometimes a “what goes up, must come down” mindset to things in the economy, and people were starting to get worried that the run-up in prices at the time would precipitate a corresponding drop, if not an outright crash. As I predicted in that August 2021 article, a housing crash did not happen, and, in fact, home prices have continued to rise.

But half a decade later, the housing market is different. The average 30-year fixed mortgage rate in August 2021 was about 2.9%. This was actually almost the exact all-time low. Today, the average rate is around 6.50%, down from its 2023-2024 highs, but up about a half a percentage point since the start of the Iran War five weeks ago.

The Chief Economist for the National Association of Realtors (NAR) said in February (even before the recent run-up in mortgage rates) that we were entering a “new housing crisis.” The 2008 housing crisis is still fresh in many people’s minds, so when someone credible throws around language like that, it’s worth a closer look. Are we headed for a housing crisis? Are we already in one? If yes, what does that mean? If not, what would a true crisis look like? Let’s dig in.

The Roots of the Perceived Crisis

I sometimes think of writing a book to try to explain the many layers and variables at play in the 2010-2025 housing market, but then again, who would read it? I can assure you that I’m not going to write a full book in the paragraphs below, otherwise who would make it to the end of this article? Low interest rates, an undersupply of new housing due to low rates of construction, sociological changes related to the pandemic, a changing economy: there is a lot to this story.

But here we are at the outset of Q2 of 2026. Let’s look at the stats today. In January, the number of existing homes sold was 4.02 million on a seasonally-adjusted, annualized basis. This was about a 6% drop-off from December and a tick down from the 4.08 million homes sold one year prior in 2025.

New home sales (as opposed to the statistic above, which is already-owned/existing homes) are also down this year. In January, the rate of new homes sold was 587,000, a sharp 17% drop from December, and about 13% below the rate one year prior in January 2025. The data for new home sales for February is now delayed (I’m guessing due to everything that is going on within the federal government); we won’t get fresh data on this statistic until May.

But put the existing and new home sales data together, and you get a housing market that has many fewer transactions happening today than it should in a normal, healthy market. In January 2020, which was the last comparable pre-pandemic (just barely) January, there were 5.46 million existing home sales and 764,000 new home sales for a total of about 6.224 million. January 2026’s combined total of 4.607 million, by comparison, is about 26% lower, which shows just how much the market for home sales has slowed.

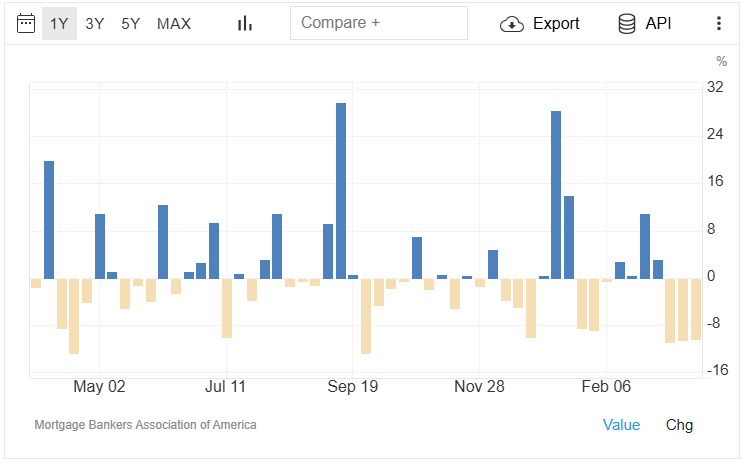

Keep in mind, too, that the NAR crisis quote was given in early February, and conditions for homebuyers have only deteriorated since then with a recent rise in interest rates. The chart below shows weekly changes in mortgage applications via the Mortgage Bankers Association (courtesy of Trading Economics). Mortgage applications were up four weeks in a row in February, but have subsequently declined by 10.9%, 10.5%, and 10.4% over each of the past three weeks (the three downward yellow bars on the far right of the chart):

The State of the U.S. Homeowner

What the data above suggests, for sure, is that the number of home transactions is going to continue to be tepid if not drop in the weeks ahead. Fewer applicants for home loans in March means fewer transactions in April, May, and June. I can understand from the perspective of a realtor how this could, indeed, feel like a crisis. It is entirely a different question, however, as to whether the housing market is actually in crisis territory.

The big problem in the 2008 housing crisis was that financial peril among U.S. homeowners triggered not only their own serious financial issues, but also systemic stress. Massive banking losses, which threatened to (and, indeed, did in many ways) rip through the economy with contagion speed led to an outright financial collapse second only to the Great Depression in magnitude in recent history. When people’s variable interest rates increased and their property values declined, many homeowners suddenly found themselves upside down on mortgages they could not afford. Defaults spread through complex collateralized debt securities, and, essentially, all hell broke loose.

Today, however, the situation is much different. True, turn on the TV or scroll your phone and there are a million reasons to be fearful in the current economy and with the state of the world right now, but any sort of systematic problems or perils in the housing market are just not showing up in the data, at least not yet.

Delinquency rates

Existing U.S. homeowners are remarkably stable, at least as far as their homes are concerned (lots of people are struggling in other areas with rising costs, particularly with gas prices in recent weeks). The delinquency rate on single-family home mortgages in Q4 of 2025 was 1.78%, a historically healthy number, and essentially where it has been for the past three years. Delinquency rates peaked recently at 2.83% in Q3 of 2020 (the heart of the pandemic), but even that was nothing compared to the 10%+ delinquency rates we saw from the end of 2009 to the middle part of 2012. I didn’t work in banking at the time, and I’m glad I didn’t. If you were to extrapolate a 10% delinquency rate onto any bank’s current loan portfolio, needless to say it would be pretty devastating after operating in the 1.0-2.0% range for the past several years.

This data shows that homeowners are generally able to keep up with their payments. However, there are also some causes for concern deep in the data. Delinquency rates are higher, for example, for less well-qualified borrowers. This is to be expected, but the numbers are fairly stark. For Non-QM/Non-Prime 2.0 loans, which is a jargony way of saying mortgages to borrowers who may not typically fit a bank’s traditional underwriting model including those who are self-employed, high-net worth borrowers with irregular cash flow, or those with irregular credit issues like a recent divorce, the 30-day delinquency rate is all the way up to 7.26%, per Fitch Ratings. That is pretty high. Delinquency rates are also higher on mortgages booked from 2023-2025, which were generally done at higher price points and with higher interest rates. There is an important story here about the K-shaped economy, and how much harder the housing market is for people who have just been getting into it as compared to those who have been there for awhile.

One reason why American homeowners are, generally speaking, not in any type of peril comparable to 2008 is that homeowners today have stronger equity in their homes, again, generally speaking. Only about 3% of homeowners are seriously underwater (i.e. they owe more than their houses are worth), per the researchers at ATTOM. By comparison, 44.6% of homeowners are what ATTOM calls “equity-rich,” which means their loan balances are half or less than half of their estimated home market values. Home prices would have to drop pretty substantially for most homeowners to be upside down, and, indeed, about 40% of all homes are paid off, which makes those homeowners particularly stable, needless to say. It’s harder to have contagion peril spread through the banking system as mortgages blow up when 40% of homeowners don’t even have a mortgage to begin with. In 2008, on the other hand, 68.4% of homeowners had a mortgage, oftentimes with variable rates which were moving in the wrong direction on them.

Is There an Actual Crisis?

I do not think the sentiment behind the “new housing crisis” quote is accurate. I wrote five years ago that 2021 was not 2007, and neither is 2026. But that doesn’t mean there aren’t some major issues out there that represent some real risks to the broader U.S. economy as a result of what is happening in the housing market.

The portion of GDP that is attributable to the core housing market (e.g. new home construction, renovations, brokers’ commissions, etc.) is about 4%. But the impact to GDP gets bigger when you factor in banking, furniture, utilities, and housing-related services; it’s in the 15-18% range. When things slow down in an area of the economy that touches nearly 20% of things, it’s going to be felt more broadly.

The threat to the economy in the current housing market is not a massive drop in prices and the contagion effect of busting mortgages, but rather that a damp blanket is put over everything as housing slows down. When fewer transactions take place, there is less money flowing and multiplying through the economy. And that is probably what the National Association of Realtors is reacting to, and why their Chief Economist is warning of a crisis. Again, I think crisis is probably a hyperbolic term to use at the current time and the NAR certainly has a vested interest on behalf of its members of juicing the wheels of things, but it’s also fair to wonder how the economy is going to look if the sluggish housing market doesn’t pick back up.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Thoughts and opinions here do not represent First National Bank.

In Memoriam

Sadly, a regular reader and subscriber to The Sunday Morning Post, Andy Molloy, passed away last week after a battle with cancer. Regrettably, I only got to know Andy in recent years. I wish I had met him sooner. We would get together every few months for breakfast or lunch at the A1 Diner in Gardiner, Maine and he’d tell me everything that was going on in the Maine media scene, state government, and more. He would pick my brain about banking, and wanted to know what every community bank in Maine was up to. I will miss our conversations greatly, and always appreciated how much he supported me and my own experiment here in journalism. Rest in peace and thank you, Andy Molloy. Read more about Andy here and here.

Excellent article. Here are my rambling thoughts…I would guess that a substantial percentage of those 40%of homeowners without mortgages are seniors with incomes that decline with increased inflation. Home repairs become a significant financial concern in those situations. A repair such as a new roof or even painting a house can result in an expense of $20,000 or more, which often requires an equity loan. As I live in an area where there are many low income seniors who own their home, their inability to keep their houses in good repair has an impact on the local economy that is not seen in any statistic that I know of. For seniors able to qualify for a loan, their debt for maintenance, and struggles to make those payments, can become significant. I guess what I’m wondering is, is their debt reflected in the housing statistics? Rather like during the feudal period when the landed lords were able to live well, the vast majority of the population were serfs who struggled to save enough wheat for themselves after paying the landlord their rent portion. The only statistic that was important to the king was that the Lords were doing well while the surfs were outside of his concern.