Home Construction Slows Exactly as More is Needed

An unfortunate thing has happened on the road to recovery in the housing market, which is that after a boom in construction from 2020-2022, the rate of new home supply has started to once again go in the wrong direction. Is this recent reversal a temporary blip, or is it the start of a new multi-year trend? And what can policymakers do to boost new construction back in a positive direction?

But first, a mini-history lesson on how we got here to begin with. Rapidly rising rents and soaring home prices did not happen out of the blue. The reasons for the spikes coincided with the pandemic and, to be sure, were enhanced by pandemic-related activities, financial realities, and movements of people. The Federal Reserve lowering interest rates to historical lows in March 2020 and holding them there for 2+ years certainly gave tailwinds to an exuberant housing market, as well.

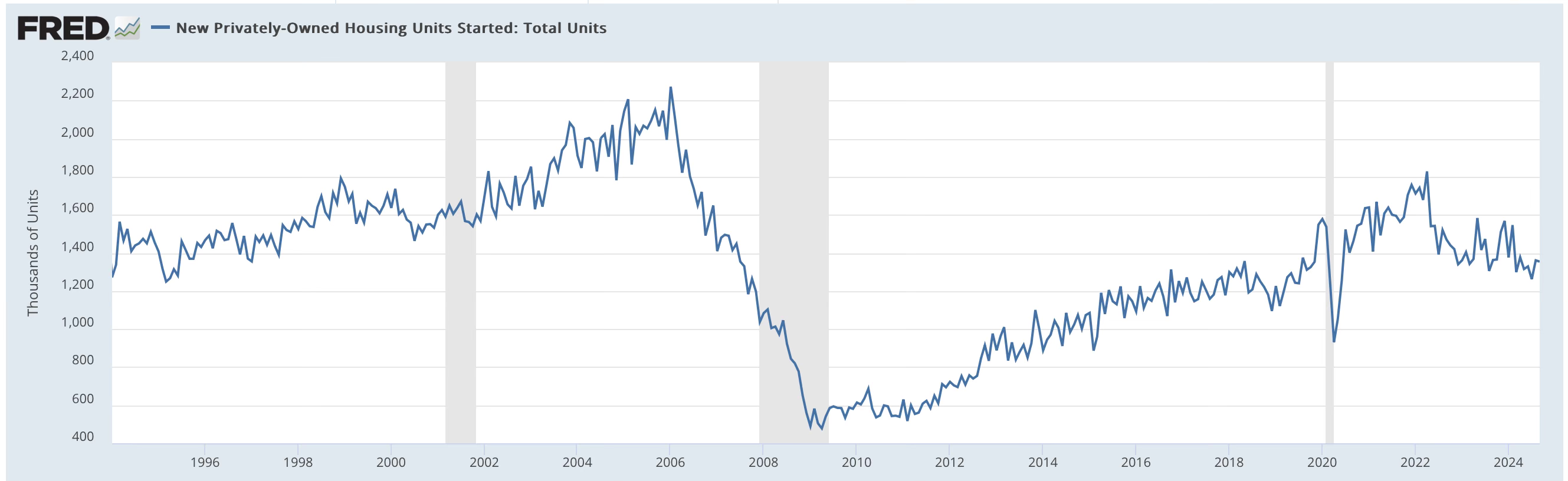

But, long-time readers of the Sunday Morning Post will know that the roots of the current housing crisis began during a period of significant under-building from 2009-2013+ following the depths of the Great Recession. The chart below shows the data for new housing starts over the past 30 years. The drop during the Great Recession is clearly evident, and despite an overall economy that was recovering for much of the last decade, new housing starts never recovered to their pre-2008 levels. The gap in new home construction from 2009 onward has played itself out in higher home prices today from lack of supply.

But What Now?

Sharp-eyed chart observers will note that after a fairly steady run-up in new housing starts over the past 15 years, the trend over the past two years (the far right side of the chart) has been that of a reversal. The rate of construction of new homes in this country as of September was 1.354 million homes (annualized and seasonally adjusted). This is down from a peak of 1.828 million homes in the spring of 2022, a drop of just over 25% in the past 18 months.

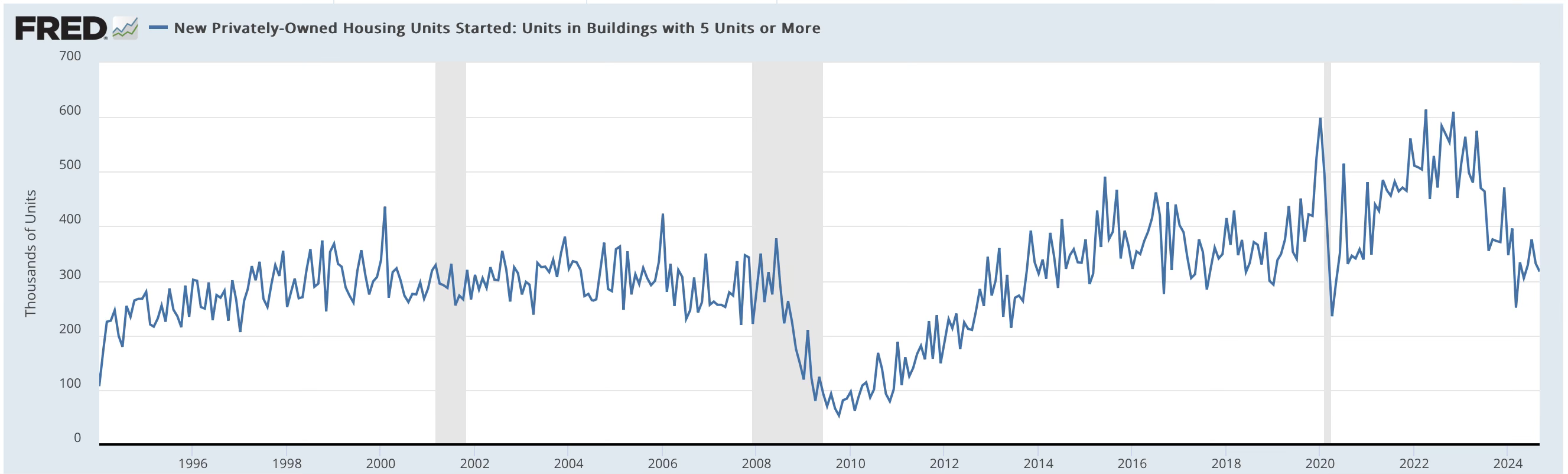

The story is a similar one in multi-unit construction. In fact, the chart of multiunit construction below looks very similar over the past 30 years as the chart for single-family construction, including both the rebound following the Great Recession (although it was a more robust rebound than in the single-family market), and a decline over the past year or two that mirrors the decline in single-families:

As of September, multiunit construction was happening at a pace of just 317,000 units/year (annualized, seasonally adjusted), which is almost half of what it was in 2022.

Why is construction down? There are several reasons. First, construction dropped at the same time interest rates climbed. Not only did this slow demand among new would-be homebuyers looking to build, but builders, much like ordinary consumers, are also subject to the math of high interest rates. When the interest rate for a builder who is financing their project starts with an 8 instead of a 4, fewer projects are going to be done because the math just doesn’t work as well (or at all).

Second, inflation has hit the building trades market. While some supplies and certain materials have come down in price from their pandemic, supply-chain induced peaks, other costs of development are higher including insurance, contracted labor, permitting, and engineering. With all of those costs going up (in addition to high interest rates), it makes the math of building even harder.

Third, the labor market is very tight. As noted above, the cost of labor is higher as builders have to pay their teams and subcontractors more to complete projects, but beyond that, there just aren’t enough workers to go around. I speak to a handful of builders regularly in my own local market, and each one of them says they could compete many more home construction projects if they just had the people; the demand is there, but the workforce is not.

Lastly, I think especially in the current year, there has been a lot of uncertainty out there. Much of that is election-related. You can talk to almost any small business owner, construction or otherwise, and they will tell you that business slows down in the month or two before a major election. It is like consumers are just frozen in place, waiting out the results. I think for much of the 2024 calendar year, consumers have been treading water on major life decisions including whether to build a new home.

What Comes Next

The Fed Chair has said numerous times that the Fed’s purpose is not to ensure a healthy housing market. That may sound callous, but the Fed is specifically charged with supporting full employment and limiting inflation, not facilitating equilibrium in the housing market. Chair Powell has pointed to Congress and other policymakers as the ones who have to pull their own levers on housing if they want to make a difference.

So what levers can be pulled? The government itself could build housing, which is happening in different places through quasi-governmental relationships with local housing authorities and others in the private sector. The Biden Administration has had various policies and proposals to provide financial assistance in the form of down payment assistance or reduced interest rates for first-time homebuyers and those from traditionally under-represented demographic groups. It remains to be seen what Trump will do on that front (probably not much, as all indications are that he will be attempting to hollow out the federal government and not enhance what was done under Biden).

Beyond that, and a bit beyond the scope of today’s article, cities and towns and other jurisdictions can address their zoning rules and regulations to incentive more construction. Other ideas include building on federal lands, and incentivizing builders on the supply side rather than just supporting buyers on the demand side, and still further creative ideas.

For now, however, the trend downward in construction is unfortunate and ill-timed, as shelter (both homes and rents) continues to be one of the most robust categories of inflation in the Consumer Price Index. Ultimately home prices and rents will come down one of two ways: either the economy falters and prices come down as a reflection of decreased demand (and a lower ability of tenants and homeowners to keep up with their rents and mortgages), or the supply of homes and apartments increases so notably that rents and home prices come down due to saturation of supply. With the recent downtrends in construction, however, it appears the latter option is not especially likely barring some re-reversal in the form of a construction boom over the next few years. Time will tell on the economy.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com.