Housing Inventory Jumps

Two key pieces of recent data suggest the housing market is showing further signs of stabilizing after a frenzied few years. This comes with a caveat of particular interest (and frustration) to would-be buyers that prices and interest rates remain elevated, although there are signs there, too, that some normalization is on its way, especially in certain markets. But there are other key data points that show the housing market has reverted to its pre-pandemic norms, which could soon lead to an easing of prices. Let’s dig in.

Inventory + Days on the Market

In July, there were about 1.1 million homes listed for sale in the United States, per data from the National Association of Realtors via FRED. That is about 216,000 more than there were one year ago in July 2024. That is an increase of nearly 25% in one year. The increase over two years ago? 70%! There are about 453,000 more listings today than in July 2023. Believe it or not, if you look at the "low July,” in recent history, which was July of 2021, during which month there were only about 547,000 total home listings, the increase is almost exactly double in four years. In other words, there are twice as many homes for sale today than there were four years ago.

Now keep in mind that we are still about 11% lower than July 2019, and it’s easy to “data-fit” a hypothesis by choosing an abnormal low to compare against, but there is no doubt about it — inventory is climbing.

A big piece of the inventory puzzle is the listing of new homes for sale. The seasonally adjusted total of new one-family homes for sale in the United States hit a nearly 18-year high in June. The last time single-family home listings were as robust as they are now was in October 2007. I talk to a lot of homebuilders regularly. Many had been expecting a slowdown in new home construction projects as the pandemic surge petered out and as interest rates rose. It seems the construction boom still has legs, however, as most of the homebuilders I talk to say they remain very busy. The major impediment to even more construction is a lack of labor and, at times, onerous local approval processes.

Median Days on the Market

So what we are seeing this summer is more existing homes for sale and more newly constructed homes for sale. This leads to another housing statistic that has also returned to its pre-pandemic normal range, and that is the median days a home listed for sale stays on the market. In July, the average was 58 days, or just under two months. By comparison, the average was 51 days in July 2024, 45 days in July 2023, and just 34 days in July 2022. In July 2019, it was 57 days, so the statistic is just about the same today as it was pre-pandemic.

This data matches what I am hearing from realtors lately — homes are staying on the market for longer. This is a result of two related factors. First, buyers have more options due to the greater levels of inventory, so they can be more choosy. Second, buyers are not as aggressive in general because the math continues to be very challenging due to high interest rates and high prices, not to mention a general sense of economic uncertainty out there. As a result, homes for sale are sitting for longer. This means sellers must be patient and perhaps not price quite as aggressively to the high side as they would like. It also means that realtors are generally working harder to sell listed homes, and to help guide buyers through the process. Although that process is generally taking longer, the positive side of the coin for realtors is that with higher inventory as a whole, there are more available options to sell.

What Comes Next

If you’re a buyer, the market should be looking more attractive, although perhaps only incrementally so at this point. At the very least, there should be more options to look at, and the homes that are listed should not be subject to the same fierce bidding wars that were so common several years ago.

If you’re a seller, on the other hand, it may feel like this market is starting to turn on you. It’s a lot easier to sell your house when it’s the only one on the block or one in the neighborhood for sale. But when there is a similar home down the street that is also listed, the pricing war can start to move in the wrong direction for a seller. Sellers may need to price less aggressively, and also be more patient as the data suggests that the house that sold in one month last year is taking two months to sell today.

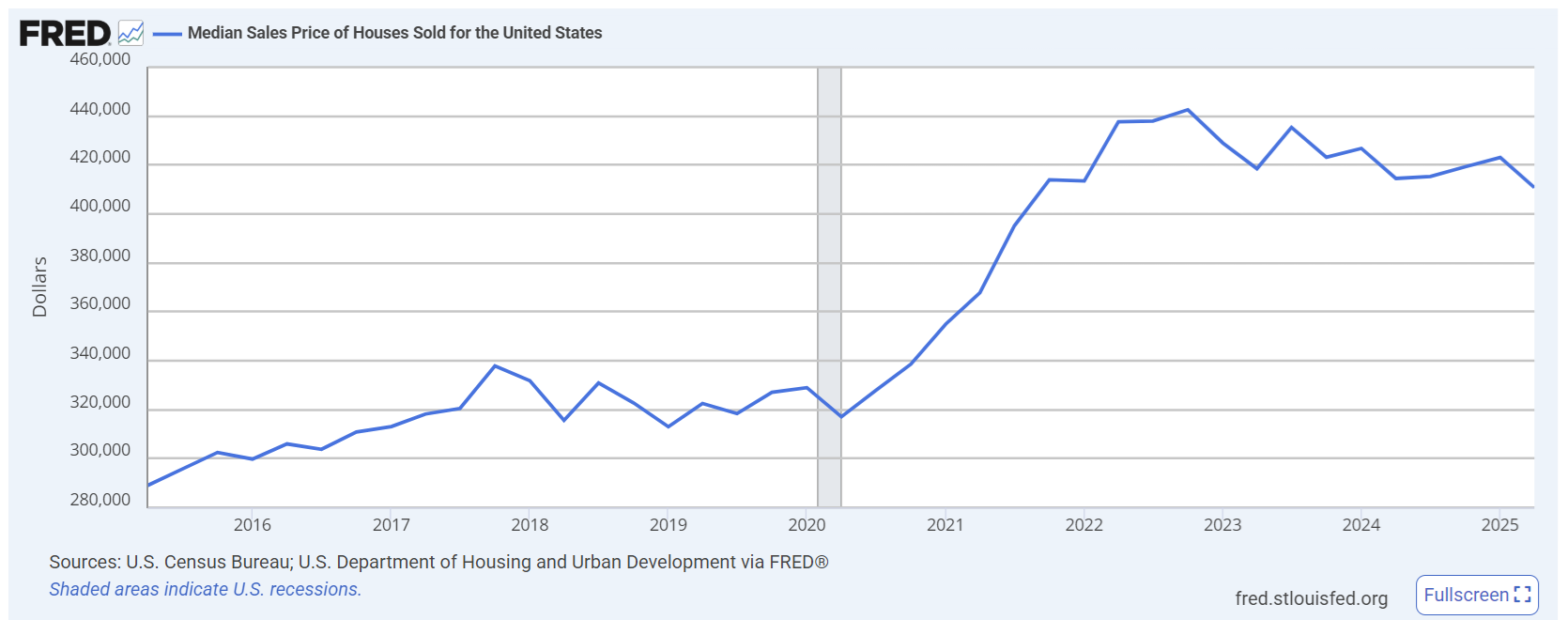

I said in my housing market preview for 2025 that I see home prices modestly dropping this year. The chart below shows the median home prices of homes sold nationwide according to the U.S. Census Bureau and HUD. According to their metrics, home prices peaked around $442,000 in 2022, and have already eased down to about $411,000 today, a drop of about 7% (although, to be fair, other well-regarded data sources including the S&P Case Shiller Index show prices that are continuing to modestly rise). The Census/HUD chart does look compelling, though:

Houses are a unique “widget,” to use a common Economics 101 term, but home prices are still subject to the same laws of supply and demand. When the supply of something increases, prices tend to drop (even if demand remains steady). But we are in a unique moment where supply is increasing and demand is perhaps easing down (or at least dormant) as would-be buyers wait on the market. For these reasons, I see home prices continuing to decline — you have two levers (increased supply and declining demand) that both should lead to declining prices. The drops will be most notable in markets in the South, Sunbelt, and West, where construction of new homes has been the most robust.

For my readers here in Maine, our real estate trends generally mirror what is happening nationwide — the median days on the market for homes here in Vacationland was 53 in July, up modestly from 47 in July 2024 and 33 in July 2023. The median days on the market bottomed out in Maine in May 2022 at an average of just 22 days, a reflection of Maine’s roaring real estate market during the pandemic, as Maine was seen as a particularly safe place to be, and an attractive one at that, especially for the work-from-home/remote-work crowds. Home prices in Maine have shown no real sign of declining, though, and, in fact, continue to rise.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com.

Have a great week, everybody!