How the Iran War Could Impact U.S. Interest Rates and Housing

As the old saying goes, a butterfly that flaps its wings in Brazil can cause a tornado in Texas. As millions of Americans (and people around the world) have experienced when pumping gas over the past two weeks, the Butterfly Effect is real in today’s global economy, although the catalyst for the updraft in gas prices has been more than just a butterfly flapping its wings, but the sudden and intense bombardment of Iran by joint U.S. and Israeli forces starting on February 28th. Whether you call it a war or an excursion, as President Trump has labeled it, the aerial attacks have launched a conflagration with uncertain aims and questionable odds for quick resolution.

Gas prices are a particularly visible quantitative metric of the impact of these events, and that impact has been suddenly and intensely experienced by people and businesses around the world. About 20% of the world’s crude passes through the Strait of Hormuz, which has long been one of the world’s most important 100-mile stretches of water (about 24 miles across at its widest point), and only the more so today.

According to AAA, the average price at the pump closed this past week at $3.63/gallon, up about 23% since before the war/excursion began. Morgan Stanley has estimated that just a 10% rise in oil prices results in a jump in the Consumer Price Index (CPI) of 35 basis points (for all intents and purposes, 0.35%). For a CPI index that has been slowly and stubbornly inching its way back down to the goal-level of 2.0%, a potential boomerang up 0.35% or more would be a frustrating move in the wrong direction.

It may seem trite to talk about interest rates as bombs are flying and, sadly, as American service members are now coming home in caskets (with at least 140 injured so far), but the events unfolding now in Iran really do have a significant impact on life here at home, so they are worth addressing.

The price Americans pay for gas is, as mentioned, one of the more visible metrics. But it is the ripple effects of high oil and gas prices that really impact things. When Americans are paying more at the pump, they have less money to spend elsewhere. For better or worse, we are a consumer-driven economy, and when people don’t go out to eat or shop or travel, the multiplier effect from spending is much more muted.

As a quick aside, I was never able to pull all the data together, but a project I wanted to do at one point was to compare attendance at my state’s local high school basketball tournament each February with gas prices. Maine is a rural state, and people need to travel pretty far to make it to one of three centrally located tournament sites in Bangor, Augusta, or Portland. I spoke with the G.M. at one of these sites years ago, and he told me when gas prices are high, they see less attendance. People are sensitive to the price of gas. That means fewer ticket sales at the venues, but less spending in the area restaurants, hotels, and shops. For many years, it was thought that the high school basketball tournament week was the best week for car sales in the Bangor area of the entire year. I’m not sure if that’s still true, but you get the point.

Businesses, too, are sensitive to energy prices, of course. Oil itself is a production cost in virtually every tangible product. Plus, think of every business that has a travel component, and not just tourism related entities, but companies that ship lots of products or make deliveries or have to move one thing from one spot to another. If your input costs are higher due to the higher cost of oil and gas, you are either going to be less profitable or you have to pass that cost along to the consumer, which results in rising prices.

And, that, ultimately, is one of the big concerns about the Iran War, which is that it is going to lead to higher prices here at home. If prices are higher, it will give the Federal Reserve pause on lowering interest rates further along the same trajectory they have been doing for the past 18 months.

The Federal Reserve meets this coming week. A few months ago, there was roughly a 50-50 chance that interest rates would be dropped by a quarter point at this exact March meeting. Today? The odds are greater than 99% that rates will not be decreased, and the odds aren’t looking that good for the next several meetings either for those looking for rates to come down. According to prediction markets, the most likely odds are now for only a single rate cut in 2027, and there may not be any.

Mortgage Rates in the Last Two Weeks

Markets have reacted sharply to what is happening in Iran. The stock market is down about 3.5% since February 28th. Oil has spiked, as noted above. You can see what has happened to home mortgage rates over the past two weeks in the chart below, which have jumped too:

Things had been going in generally an advantageous direction for would-be homebuyers or those looking to refinance; the nationwide 30-year fixed rate dropped to just a hair below 6.00% at the end of February, which was the lowest rate in over three years. But the average rate closed this past week at 6.41% according to Mortgage News Daily, which is a pretty significant jump in such a short period of time. Mortgage rates are now back to being the highest they have been since the end of last summer.

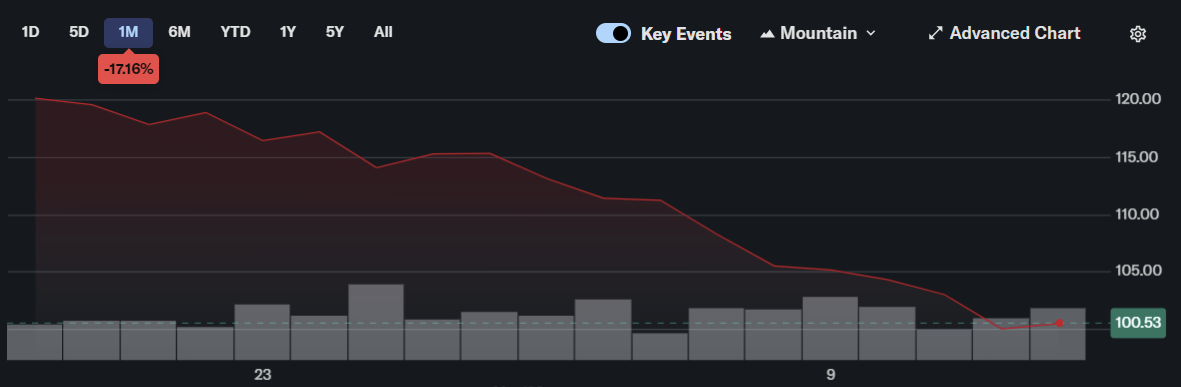

This jump in rates is bad news for buyers, but equally bad for homebuilders. A homebuilder stock index I track for insights on the general mood and outlook in the industry is down 17% in the past month, which is sizeable. Homebuilders (and those who invest in them) are feeling quite pessimistic about a potential rise in rates, as it will likely mean less construction and fewer sales:

A Possible Counternarrative

The quantitative reactions in the market to what is happening in Iran are decidedly negative. There may be one positive alternative outcome at least as far as interest rates are concerned, however. In a turbulent investment environment, there tends to be a flight to safety. For all that is happening here in the United States politically, U.S. Treasury notes are still considered to be one of the safest investments in the world. You can own 10-year U.S Treasury Note that will yield 4.28% annually right now, which in an unstable environment is very attractive to many people. The yield had been 3.94% just prior to the first attacks, which shows that the Treasury market, too, has jumped along with oil and mortgage rates. However, the longer the Iran situation lasts and the more fearful investors become, the greater the demand will be for U.S. Treasuries, and the buying up of said notes could actually bring those yields down.

There is a pretty complicated dynamic in which banks and mortgage companies tend to price their home loan rates around things like the U.S. 10-year Treasury rate. If that yield does come down, so too should mortgage rates. So in a backwards sort of way, there has been this jump in Treasury yields in the immediate aftermath of the initial attacks, but yields could ease lower in the weeks and months ahead as investor dollars pile into this safe asset, which could then have a direct relationship with home mortgage rates also coming down. At the moment, however, the immediate catalysts for rising rates (mostly due to inflationary pressures related to oil and gas) are outweighing the flight-to-safety counter-possibility.

So What’s a Person To Do?

I’ve offered some seemingly conflicting thoughts on the trajectory of future rates, and the truth of the matter is, no one knows exactly where things are going. Treasury yield rates and the rates set by the Federal Reserve often correlate with one another, but are, in fact, different things. The former is based on more supply and demand, while the latter is based on inflation, the unemployment rate, and the moods and insights of the Federal Reserve board of governors. It is highly possible that the Fed will keep rates high to fight inflation, while U.S. Treasury yields may simultaneously come down in a flight to safety by investors.

What should you do as an investor in the face of all of this? The correct answer is almost always to stay the course. But people need to be sure the risk level of their portfolios matches their own risk tolerance and objectives. We are bound to have some volatility in all types of markets — stock, oil, interest rates, Treasuries — in the weeks ahead. Investors should be mindful of this and hold the line accordingly, or adjust to a risk tolerance that matches their goals.

From my perspective, we are in for an up-and-down stock market for the next few months, with an inflation rate that inches higher from its current level of 2.4% to something closer to 2.7-3.0%, which, unfortunately, may limit the opportunity for rate declines in the borrowing sphere. That said, if the Iran War can reach a swift conclusion, there may be a snapback effect of oil and gas prices dropping significantly, which would ease these new inflationary pressures we have been experiencing over the past two weeks. Time will tell.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Thoughts and opinions here do not represent First National Bank.

I have read that about one-third of our US treasuries are owned by foreign nations with Japan, UK, Canada and China being among the top four. I wonder if the US continues its current path of serial wars if those nations’ investors will seek safer havens for their excess funds. I looked up Switzerland‘s mortgage rate for a 10 year loan and it is less than 2%.