Mortgage Application Data Shows a Sensitive Buyer

But optimism for a salvaged spring buying season.

Greetings from Newburyport, Massachusetts, where our family is spending the tail end of school vacation week. The big highlight was a Saturday down-and-back to the Franklin Park Zoo.

I have drafts of several deeper-dive pieces in the works, but for today, I wanted to draw out some data I was working with this past week that I think shows just how sensitive the buyer pool is to the current economic winds, which in the case of the past 10-14 days, have been generally favorable to the homebuyer market. This may feel surprising with such gloom and anxiety out there in the headlines, but there have actually been some signs that the spring buying season may be salvaged after things were looking pretty dismal in the late winter and early spring.

We’ll see what happens over the next 30 days, though. At the very least, moves in the data over the past three weeks underscore just how sensitive people are to seemingly small moves, but ones that actually represent some pretty big levers in the economy. It’s always worth remembering that every piece of data represents real people making real-life decisions. It’s easy to get bogged down in the quantitative metrics of it all, but you can see how significant the human impact is when you consider the actions and behaviors taking place (or not taking place) as the numbers move. Consider the following:

For all the inflationary pressures from the rising price of gas, interest rates have actually come down over the past two weeks. The average 30-year fixed rate mortgage hit its recent peak of 6.64% on March 27th, but has since settled at 6.32% to end this past week, per Mortgage News Daily. This key rate has been quite stable over the last week, fluctuating only slightly within a narrow range of 6.29%-6.33%. On a $400,000 mortgage, this seemingly small interest rate change represents a difference of about $80/month, or about $1,000/year, which is real money, especially to those just getting started out.

In response to falling rates, after four straight weeks of declines in March, mortgage applications have increased each of the last three weeks: +1.8%, +7.9%, and about +10.0% (with data for the most recent week estimated, but still being finalized). The fact that mortgage applications have so closely correlated with interest rates (i.e. as rates went up in March, applications dropped significantly; as rates have fallen over the past three weeks, applications have gone back up), shows just how closely would-be buyers monitor rates, and how sensitive buyer behavior is to changes in rates.

After some notable declines in January and February, pending home sales actually increased in the month of March, per data released this past week from the National Association of Realtors. This provides some momentum to the market as we enter the peak buying months of May through August. The home market was completely dismal in the first two months of the year, so the March number provides a little bit of optimism including to sellers looking for buyers, and for real estate agents and others in the real estate world looking to facilitate sales.

I think what has happened this winter and spring has almost been a mini-cycle within the cycle. Buyers froze up with spiking rates, yet inventory among sellers continued to increase as more homes got listed for sale. This resulted in an equilibrium shift in the market whereby a small glut of supply relative to demand combined with a pressure valve release on interest rates (i.e. the drop from 6.64% to 6.32%), plus just the normal seasonality of the housing market brought buyers back from the sidelines. It’s interesting to watch this dance between buyers and sellers, and fortunately for sellers, buyers seem to be reengaging after sitting out for a while.

It’s worth pondering why interest rates have come down. The inflationary pressure from rising gas prices has ripple effects through so many different areas of the economy, so you would think interest rates would be rising. The counter to this, however, is that in a risky economic world, there is often a flight to quality, and investors out there still see U.S. Treasury bonds as the safest and most secure investment around, so they have been pouring money into U.S. bonds in recent weeks. This has had a muting effect on key indicators like the U.S. 10-Year Treasury note, which has subsequently had a corresponding dampening effect on mortgage rates as banks and mortgage companies often price mortgages as a cushion above the 10-Year Treasury.

What Happens Next

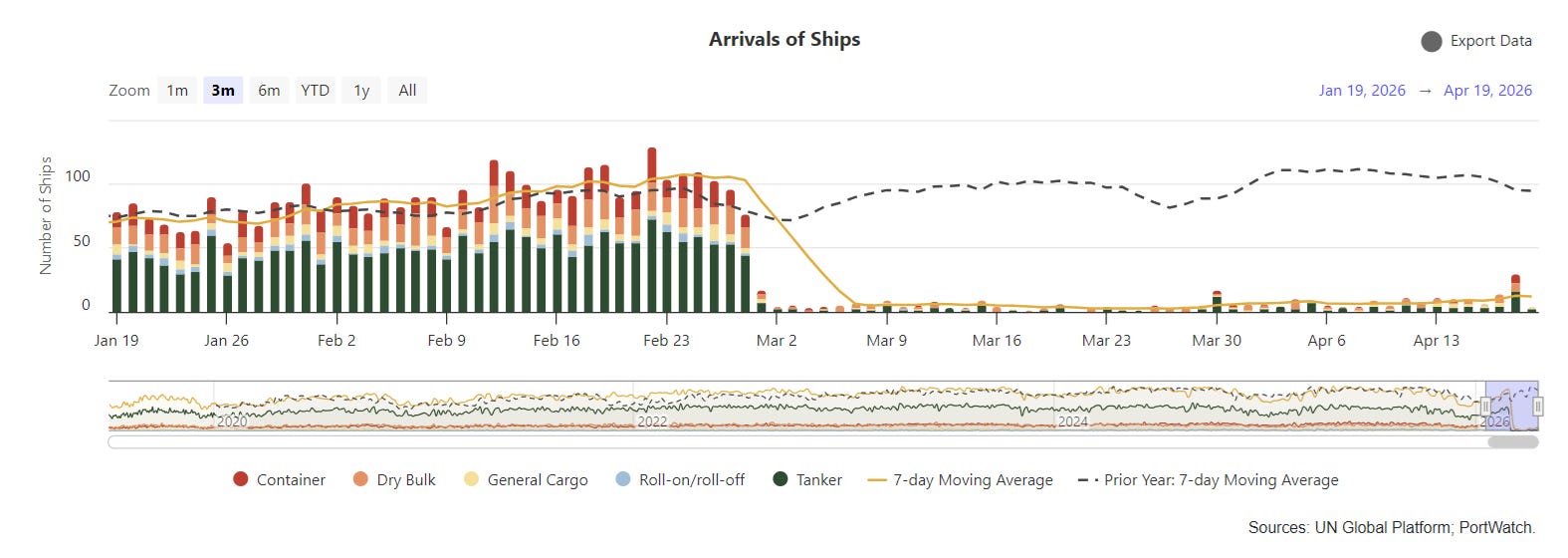

What happens from here depends a lot on the status of a fragile ceasefire in Iran and the potential re-opening of the Strait of Hormuz.

People should be aware of that chart below, and of its far-reaching implications. The chart shows the daily number of ships passing through the Strait of Hormuz. The obvious drop-off at the outset of the Iran War is clear, with an average of 90-ish ships per day crossing through in normal times and often as many as 120 or more. The number of ships passing through dropped immediately when the war began, and has been mired in a daily average of 5-7 ships for the past eight weeks with sometimes barely any ships making it through what is now a double blockade of both Iranian and U.S. ships limiting traffic.

As we saw during COVID, when global supply chains are impacted so significantly, the availability of goods and therefore their prices are altered all over the world. No doubt we will be seeing similar impacts in the weeks to come, and indeed we already are. Gas prices are the obvious one that impacts virtually everyone, but the impacts carry into other areas, too. Fertilizer prices, for example, have skyrocketed 30-50% since the end of February; about one third of all fertilizer passes through the Strait of Hormuz annually. Prices have also risen on certain agricultural goods that pass through the Strait, including corn, soy, wheat, and dairy products.

I don’t have any greater conclusions this week other than noting that the whole butterfly-flapping-its-wings analogy is real, but at this moment in time, there is more than just a butterfly flapping its wings, but a full-on conflagration in the Middle East. These things are hard to predict, to say the least. But as we’ve seen just recently, even modest moves back in the direction of stability like an extended, albeit fragile, ceasefire, help move things in a more positive direction, as with the move to the good on interest rates just recently. We’ll see what the next week has in store, however.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Thoughts and opinions here do not represent First National Bank.

It feels like we are climbing a wall of worry.