Santa's Early Gift to the 2023 Housing Market

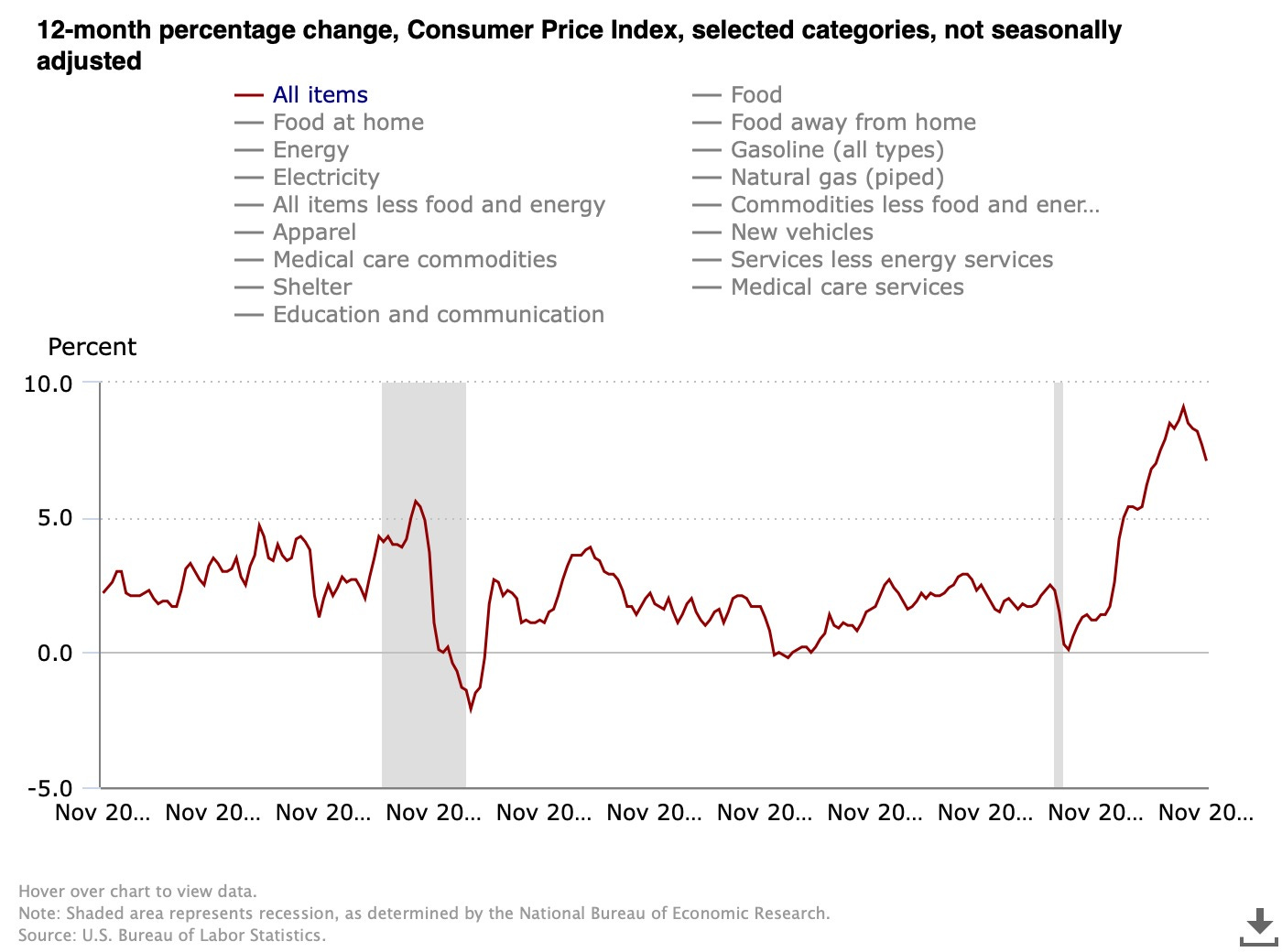

Santa Claus and his elves at the United States Bureau of Labor Statistics brought an early gift to the housing market this past week when its monthly Consumer Price Index report came out showing inflation running at a 7.1% year-over-year level. A rate of 7.1% is still pretty hot, you might say, and indeed it is. The Federal Reserve’s goal is for inflation to run at a 2.0% level. However, we now have the clear markings of a trend from when inflation peaked in June as shown in the numbers and chart below:

June: 9.1%

July: 8.5%

August: 8.3%

September: 8.2%

October: 7.7%

November: 7.1%

There is a clear reversal evident in the uppermost right portion of the chart. What do you predict the December reading will show when the data is released on January 12th? I suspect it will be under 7.00% and the trend towards inflation equilibrium will continue.

At the beginning of July, I wrote an article entitled Signs Inflation Has Peaked, in which I concluded:

I am of the opinion that inflation is peaking. I think future CPI readings will show a deceleration of inflation. In other words, inflation is going to continue to run hot and well above the Fed’s targeted rate of 2.00%, but it won’t be in the 8.00% range for many more months and

will ease back into a more manageable 4.00-5.00% range by the end of the year.That would be good news for borrowers including prospective homeowners, commercial businesses, and people seeking auto loans, credit cards, and other types of consumer debt, and, I would say, for the economy as a whole.

Well, I was mostly right, although a little too aggressive on what I thought the end-of-year inflation reading would be. I suppose there is a chance that the December data shows inflation has cooled to 5.00%, but I may have been a little premature on that part of the prediction. However, the truth of the matter is that inflation is clearly starting to settle out even if it might not feel like it quite yet.

How Does This Impact the Housing Market

The housing market has frozen up over the past few months, which is a combination of both high prices and high interest rates, a formula that adds up to especially high monthly payments on home mortgages for borrowers, which makes them more reluctant to buy. According to data from the Federal Reserve, there were approximately 526,000 existing home sales in October 2021. In October 2022, there were 371,000, a drop of nearly 30% in 12 months. Here in Maine, the number of existing homes sales dropped from 2,085 in October 2021 to 1,597 in October 2022 according Maine Association of Realtors, a drop of 23%. There are fewer transactions in every region of the country with the sharpest drop-offs coming in the American west.

The number of home sales is likely to decline further in the months ahead due to seasonality but also the fact that transactions generally lag by two or three months from when contracts were originally signed. In other words, October closings are based on purchase and sale agreements that were signed in June, July, and August, when the housing market was stronger. The brunt of the impact of higher rates, which peaked in October and November, will be felt in the housing market this winter and early spring.

However, this past week’s inflation report offers some hope in that the lower inflation reading should give some pause to the Federal Reserve as it considers whether to keep hiking interest rates in 2023. If inflation is falling, there becomes less of a need to try to reign things in by increasing interest rates. And if interest rates do not continue to climb, the housing market may be able to find some sort of equilibrium as buyers come back.

In fact, residential interest rates have actually been dropping over the past few weeks, which may come as a surprise to frustrated homebuyers who decided to head to the sidelines this summer and fall in the face of rising rates. According to Lance Lambert of Fortune, the average 30-year fixed mortgage rate has dropped by a full percentage point in the past month:

Tyler Marr of Redfin reports a notable uptick in buyer demand as represented by mortgage applications:

I plan a full 2023 housing preview in the weeks ahead along the lines of last January’s 2022 housing previous, which you can read here to see what I got right and what I missed. But after a very sluggish market over the past few weeks, there is at least some recent evidence that things might stabilize.

Addendum

A recurring theme in this newsletter is the concept of patience, and about how to invest with a contrarian mindset along the lines of the famous investment axioms, “The best time to invest is when there is blood in the streets,” and “Be greedy when others are fearful, and be fearful when others are greedy.”

Admittedly I did not think to make these investments at the time and probably would have argued against them. Plus hindsight is 20-20. But consider homebuilder stock prices including KB Homes, D R Horton, and Lennar Corporation since peak inflation in June. They have all surged:

I don’t think many people were thinking this past summer that the immediate to intermediate future was too bright for homebuilders, but look at the gains! One key lesson is that bad news gets baked into stock prices well in advance of the bad thing actually happening. And actually all three of these stocks were down considerably in the early part of 2022 as consternation about the state of the home construction market started to boil. But bad news can get overbaked, though, as a stock becomes what is referred to as “oversold.” When that is the case, bounce-backs can be significant.

Another lesson here is that buy-and-hold is still a pretty good method when investing in stocks. I am sure a lot of people who experienced the drop in value of these various companies over the first few months of 2022 gave up in the face of an increasingly gloomy home construction outlook, liquidating their holdings in the process. As the charts above indicate, however, anyone who sold their homebuilder stocks this spring or summer subsequently missed out on a significant rebound. Patience in investing means not just holding off from the latest fad, but also holding through some downturns in order to achieve the gains.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram. Opinions and analysis do not represent First National Bank. © Ben Sprague 2022