Single-Family Home Construction Plummets; Multi-Family Construction Remains Active

Greetings, readers. Thank you for being here. I hope everyone had a nice Thanksgiving. I have been busy this week visiting with family, getting Christmas decorations down from the attic, and also taking care of my children, two out of three of whom seem to have come down with whatever flu bug is going around. So I have a shorter-than-usual piece this week, but it contains some interesting data that shines a light on a complicated and increasingly perilous construction market. Check back next week for more content and stay healthy out there.

Single-Family Home Construction Plummets; Multi-Family Construction Remains Active

Data released last week by the Commerce Department showed single-family home construction down by 6.1% as activity dropped in all four major regions of the country. Additional data showed homebuilder confidence down for the 11th straight month and sitting at its lowest level since June 2012 other than during a brief period of time in the spring of 2020 at the outset of the COVID-19 pandemic.

One year ago in November 2021, 1.2 million homes were being built on an annualized basis. In October 2022, however, the most recent month for which data is available, just 855,000 homes were being built annualized. The drop over the past year with particular acceleration as interest rates started to rise in April is shown in the chart below:

Mortgage rates are the most obvious culprit for the drop, as the nationwide 30-year fixed rate mortgage is currently sitting around 7.00%, a rate not seen since 2002. This has priced many buyers out and led others to take a pause. But Americans are also worried about inflation, early cracks in the labor market, and a stock market that has swooned this year. People are feeling hesitant to make big life decisions, like building a new house. The two-year pandemic-induced housing fever has broken and the housing market is grinding to a standstill. I spoke to one local real estate agent this week about an open house she was holding and I asked how many people showed up. The answer? No one.

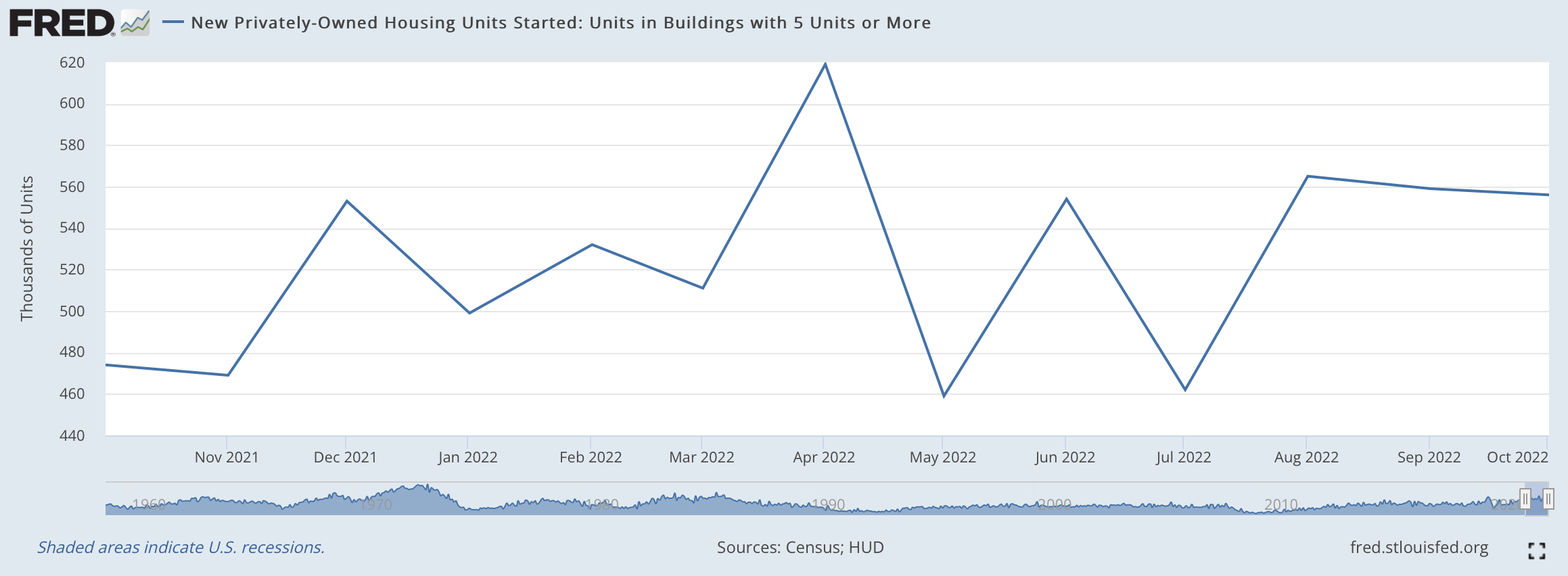

What has not halted quite so immediately, however, has been construction of multiunit rental properties. Although there is a little bit of choppiness to it, the trajectory of the line in the chart below is decidedly different than the shape of the line in the single-family home construction chart above:

In November 2021, there were 469,000 multiunit rental properties being constructed. In October 2022, there were 556,000. This means that while the number of single-family homes being built has dropped over the last year, the number of multiunit rentals under construction has actually increased. While this 556,000 figure is down slightly from 559,000 in the month prior, it is still a strong figure that reflects an active market.

What to Make of it

Why the strong rental construction market? It’s the housing crunch and simple economics. Everywhere you look over the last two years there have been headlines about rising rents and a lack of housing. I wrote in January that the private sector could close the housing gap, and that is exactly what I believe is happening:

If you believe in capitalism and free markets, which I do, you might also recognize these days that the private sector is pretty actively working to close the housing gap on its own. It is a principal of economics that when a profit opportunity exists (i.e. demand among consumers is strong), the market will respond to meet it (i.e. businesses will create new supply of what is demanded). Right now demand for new homes and rental units is roaring. And the forces of supply are responding.

One’s thoughts on whether this is all positive or negative largely depends on where you sit in the current housing market. If you are a buyer who has been patient, things are looking better with regard to price, although this is tempered by higher interest rates. If you are a homebuilder or contractor, however, the slowdown in new construction reflects dampened demand from buyers, which is obviously not great. I speak to numerous homebuilders on a regular basis and most seem to have jobs booked out well into 2023, although the cancellation rate is also creeping up. According to Redfin via Business Insider, 60,000 home contracts were cancelled by buyers in October, which is a pretty big number. Nationwide, cancellation rates are above 20% in most markets and approaching 30% in some of the bubbliest.

Frustrated renters should see some relief in the months ahead as a surge in new multiunit inventory comes online. The changes in many markets may only be incremental at first, but if you take a duplex project here, the construction of a four-plex over there, the conversion of a group of single-family homes to rentals across town, not to mention larger projects with dozens of new units that pop up here and there, and then multiply those anecdotes out economy-wide and repeating over several building seasons in a row, all of a sudden the rental market will show signs of change. Tenants will have more options, they will shop around more for units, and the power in the landlord-tenant relationship may flip.

Property owners and landlords should be mindful of this. I have written about this here and there over the last year so I hesitate to dwell on it again, but the perfect storm for rental property owners would be rising interest rates, significant new inventory that spreads out the renter pool, and a potential economic recession with higher costs across the board including on utilities and capital expenditures plus tenants who are struggling to pay rent if they have lost their jobs. When projecting cash flows and writing pro formas, real estate investors should not make calculations based on the historic period we have just gone through of near-0% vacancies, low interest rates, and rising real estate values. Instead, investors need to consider greater vacancies, static or even declining real estate values, and increased competition as a result of the construction of new units. The market is changing and it may takes some time to sort out, but it is definitely different today than it was a year ago.

For the overall economy, slower construction of new homes is a drag on economic activity. There are many positive ripples when a home is built as money is spent on various contractors and labor, materials and supplies, furnishings and more. Plus transactions keep real estate agents compensated and title companies, appraisers, inspectors, and banks busy. As the real estate market slows down, it has a dampening effect on pretty big swaths of the overall economy. This is, of course, something the Fed is okay with and is even encouraging as a slowing economy will also dampen inflation, which the Fed is hawkish to control. In my opinion the path to a soft landing is still there, but particular pain will be felt by some including many in the real estate field at least until interest rates stabilize and eventually drop, the latter of which which may be still another 12-18 months away.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram. Opinions and analysis do not represent First National Bank.