Some Regional Housing and Rental Stats

Greetings from southern Maine, where I am spending the weekend with my family and my son’s U10 travel soccer team that I coach. We are here for a weekend tournament. With that in mind, I have just a quick piece today to go through some quick real estate stats.

I’m also eager this week to see Thursday’s inflation report, particularly in the context of New York Fed Chair John Williams saying last week that “we are at, or near, the peak” for rates but that it may take until 2025 for inflation to settle into the Fed’s target rate of 2.0%. We’ll see what Thursday’s CPI report has to say, especially on the heels of what was essentially another quite positive jobs report last week, showing there were 336,000 new jobs in the economy in September.

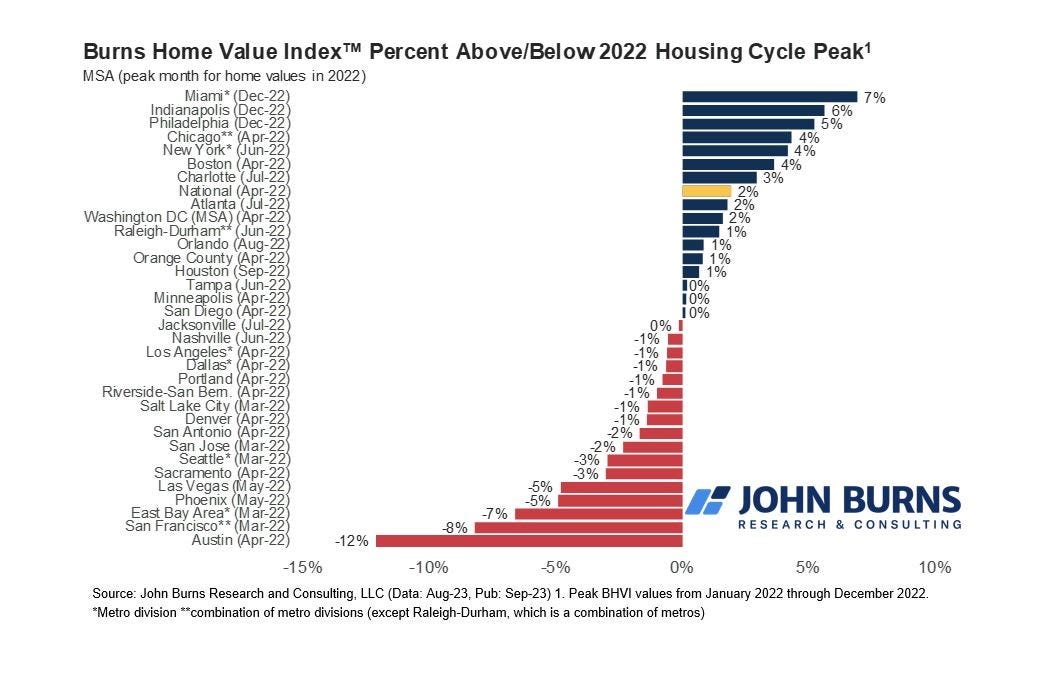

As we turn past the last quarter post of the year and head into the final straightaway towards 2024, there are some interesting things happening in the real estate market across the country. According to the National Association of Realtors, even as interest rates hit their 20-year highs, home prices in August were still up nationwide by 3.9% to a median price of $407,100. However, the term “nationwide” can belie the fact that regional differences continue to entrench themselves in the data. Consider the chart below via John Burns Research & Consulting, which shows how August 2023 home prices in various markets across the country compare to peak prices in 2022.

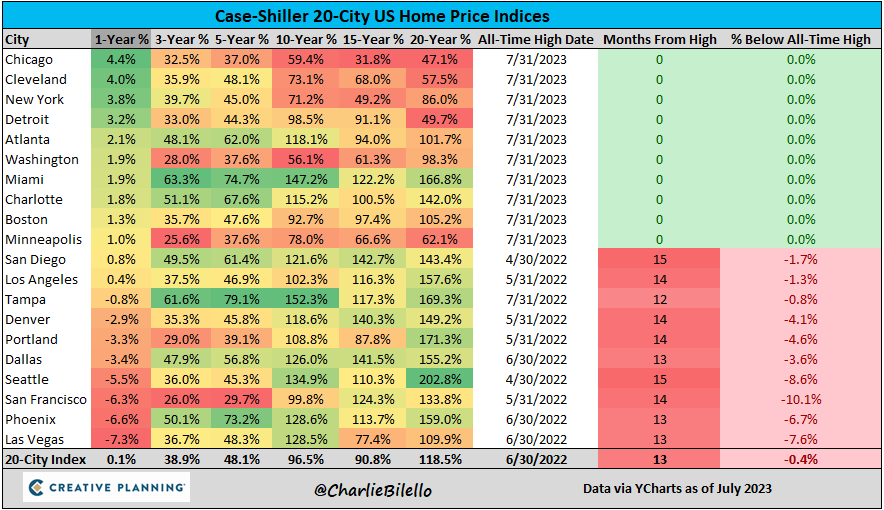

Almost all of the markets that have seen continued price growth in 2023, which are represented by the blue bars above, are located in the East. Nearly all of the markets that have seen price drops in 2023 compared to their 2022 peaks are in the West and Southwest. Data below from the Case-Shiller Home Price index via Charlie Bilello on X (formerly Twitter) shows the same basic geographic differences, with cities in the Midwest and East showing year-over-year growth while cities in the West and Southwest are down:

What gives? Well certainly there are specific variables at play in each market (i.e. politics, climate, etc.), but what is generally playing out is a swinging back of the pendulum from cities and regions that saw the biggest run-ups in prices during the COVID-era. These price surges were often due to migrations of people out of the big tech-centers to nearby smaller cities like Phoenix and Dallas not to mention the most trendy “work-from-home-for-the-lifestyle” places like Austin and Nashville.

If you’re a prospective seller in Phoenix, Dallas, or Austin, the drop in prices this year might be more than a little concerning. Although the decline is in many ways simply the market trying to find equilibrium: a drop coming off of an artificially high peak does not necessarily mean there is anything inherently “wrong” or broken about these real estate markets, it is just a correction back to the norm. And, in fact, if you look at the Case-Shiller chart above, the markets that have seen the biggest drops in the last year are also the ones that have seen the biggest gains over the past 10, 15, and 20 years. But still, sellers in these markets have to be feeling a little anxious.

What about the Rental Market?

The topic of rent prices is something I plan to come back to in more detail soon for a deeper piece, but just to touch on it today, rent prices nationwide were basically flat through August. But as with home prices, there are regional differences. According to Kim O’Brien from RealPage, the Northeast is still seeing the strongest year-over-year rent growth at 3.1%. But as you can see in the chart below, the COVID surge in rents is reversing for sure both in the Northeast (orange line) and nationwide (green line) after a notable, atypical surge during the pandemic. This is good news for tenants, but something for rental property owners to be mindful of:

Adding to the rental story a bit, Jay Parsons recently noted on X, of the top 50 metro markets, only six saw year-over-year rent growth of 3.0% or more (Newark, Cincinnati, Milwaukee, Chicago, Boston, and Kansas City). Parsons offered that the common variables in the communities that have seen the highest growth are:

1) Much lesser new supply. 2) Northeast and Midwest regions. 3) College towns. 4) Energy markets. 5) Mostly smaller metro areas.

Of note to my Maine readers, with rents jumping by 4.3% in the past year, Portland, Maine ranks #15th in the country.

What Comes Next

With high prices and high interest rates, I fully expect home prices to decline in markets across the country. There is still more decreases to come in the markets that got overheated from 2020-2022, and eventually things will level off in the Northeast and Midwest and those markets, too, will see price drops. As for the rental market, continued creation of new supply should lead to a further easing of rents as prospective tenants are met with more available options on the market. Although to be sure, those same high interest rates will likely lead to a cooling in construction of new units as developers find it harder to borrow. Stay tuned for more on this latter topic. I am waiting for some fresh data and will publish some additional analysis in the weeks ahead.

Weekly Round-Up

Here are a few things that caught my eye this week:

Via Lance Lambert, 30-year mortgage rates hit a (gulp) 23-year high, topping out on Friday at 7.84%. The 10-year Treasury also hit 4.88% on Friday before settling in at 4.795% to end the day. A risk-free annualized rate of return of 4.88% for ten years is something that would have been virtually impossible a year ago.

Will Manidis had a thread on X purporting to be able to outperform most investment funds by investing in…Legos. Read it here.

The U.S. Supreme Court declined to take a case brought by two landlord associations in New York City, who wanted the Court to strike aspects of a 2019 New York law that limits rent increases. The Court did not offer a reason for rejecting the case, as is their custom, but it is believed to be a blow to the landlord and property owners that the case was not accepted by the Court. Read more here.

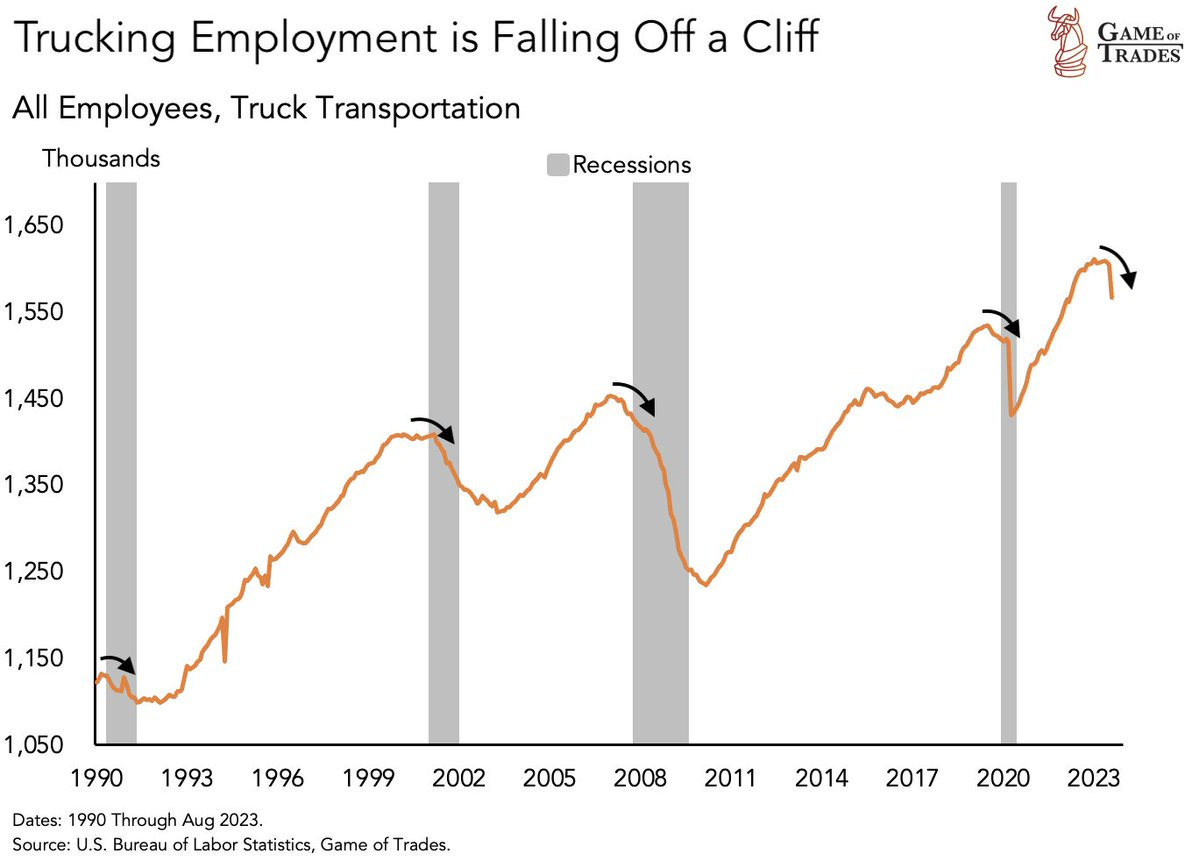

Game of Trades has a chart showing that declines in trucking employment are a common leading indicator that a recession is on the way. It looks like the signal is flashing for sure:

Have a great week, everybody!

Ben, do you have any comments on why Chicago is seeing price appreciation?