The First Cracks in Inflation?

As the Federal Reserve tries to cool rapid inflation by hiking interest rates, which may include potential increases of 50 basis points at a time (0.50%) as opposed to the usual 25 basis points (0.25%), the hope is, of course, to achieve a Goldilocks not-too-not, not-too-cold equilibrium. It would be nice for the plane to ease onto the runway by merely raising the spoilers on the wings and adding some rearward thrust as opposed to crashing the nose into the ground, in other words.

This coming Tuesday, April 12th, at 8:30 am is when the next monthly report on inflation from the Bureau of Labor Statistics will be released. The report will offer numbers for the month of March. I will be watching it closely to see if there is any evidence of stabilization following last month’s reading of 0.8% on a month-over-month basis and 7.9% on a year-over-year basis.

The chart below illustrates the steady rise in year-over-year inflation over the past year. Keep in mind the Fed’s target inflation rate is 2.0%:

Peak Inflation?

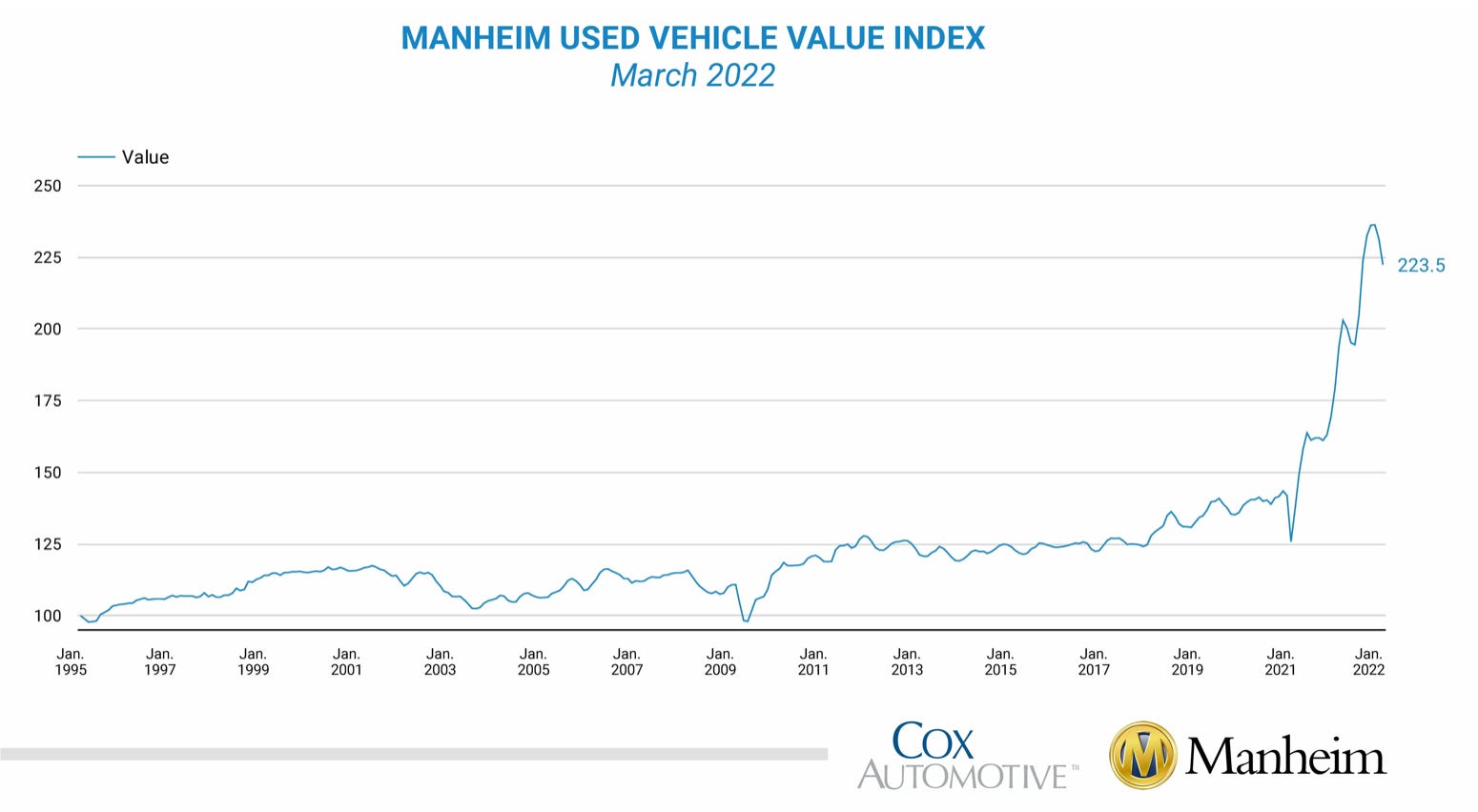

Despite the rapid rise, there may be some evidence that we are approaching an inflection point in the inflation conversation. Consider this: used car prices actually dropped in March by 3.3% on a seasonally adjusted basis. This was the largest monthly decrease in nearly two years. Now, to be fair, prices in March 2022 were still significantly higher than they were in March 2021 and March 2020, but the rate of increase not only eased, but it actually (very) modestly reversed. The chart below of the Manheim Automotive Index, which tracks used vehicle prices, shows just how significantly used car prices rose during the pandemic:

From the archives: I’ve written about lumber bubbles and tulip bubbles in the past.

This sure looks to me an awful lot like a bubble that is about to burst.

Why does the price of used cars matter so much? Well, not only it a sign of a product that may be normalizing as supply chain issues loosen up, thereby bringing more available car inventory to market, which should ease prices a bit as supply will finally be able to catch up with demand, but used cars themselves are one of the product variables that goes into the actual CPI readings on inflation. If used car prices can get under control and even reverse, it will help ease the overall inflation reading. According to the Bureau of Labor Statistics, used cars are actually represent 4.143% of the overall CPI inflation reading. If used car prices drop, it will act like those spoilers on the wings, helping to slow down the overall plane a bit.

Gas Prices

Significant conclusions should not be drawn off of short-term data, yet it is notable to me that the increase in the price of gas in the United States has halted and, in fact, somewhat reversed over the past 3-4 weeks. According to AAA, the average price for a gallon of regular unleaded right now is $4.123, down about 4.80% from a peak of $4.331 on March 11th. This provides some hope to consumers at the pump, but also slightly eases the costs of doing business for all types of entities that have to pay for fuel (e.g. freight, transportation/travel companies, etc.). The fact that gas prices did not continue their rapid ascent is a positive signal on the inflation front.

House Prices

According to the analysts at Redfin, there are some signs of (very) modest cooling in the home purchase market:

Fewer people are starting online home searches and applying for mortgages than this time last year, and year-to-date growth in home tours remains far below 2021 levels. An increasing share of sellers are also reducing their prices after putting their homes on the market.

These adjustments may be attributable to the fact that the rate on the average 30-year fixed mortgage in the United States continues to push towards 5.00%, which should slow down purchasers a bit:

Anecdotally speaking, what I have been seeing lately has been a surge in interest among prospective borrowers who are looking to lock in rates before they rise. I expect in the intermediate term the higher rates will cool things off a bit.

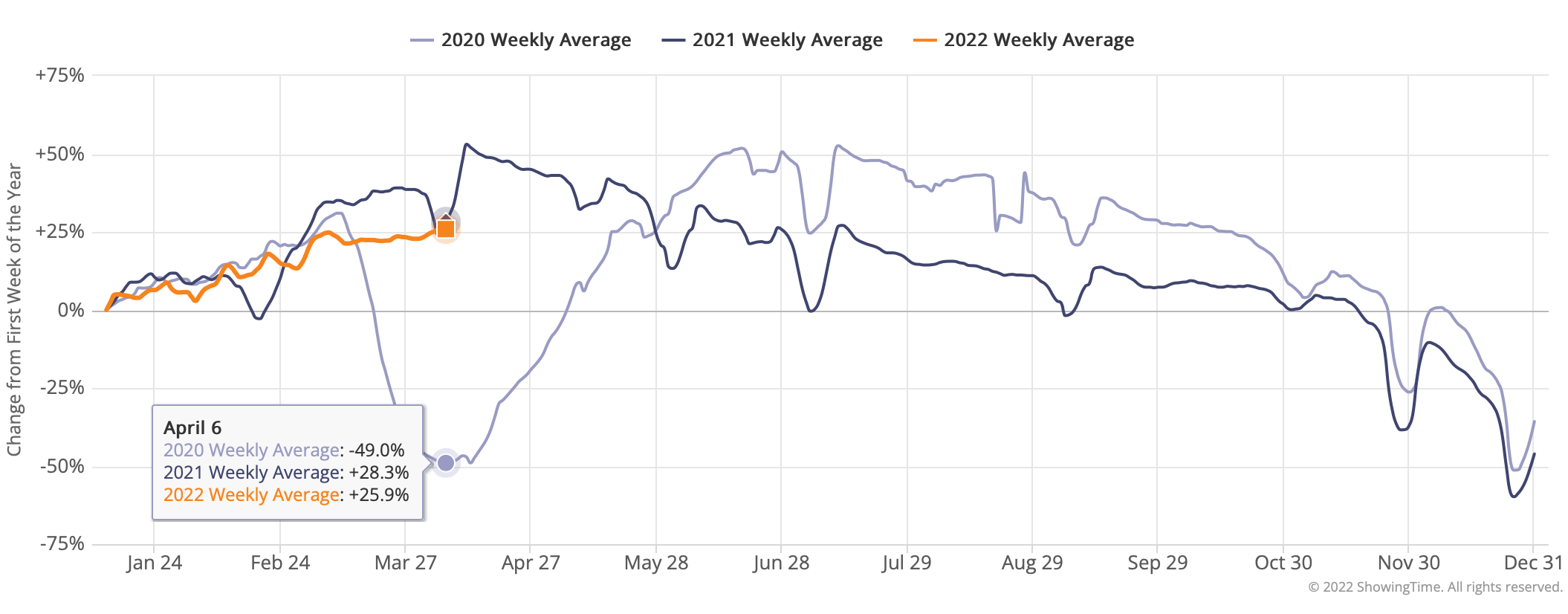

I have never seen the following piece of data before prior to reading about it this week, but the chart below shows the number of real estate showings throughout the year as compared to the first week of January each year. The trajectory of the chart is a little bit confusing, but it illustrates that showings do tend to increase this time of year versus the dead of winter, but the rate of increase in 2022 so far (+25.9%) is actually less than the rate of increase in 2021 (+28.3%), with 2020 as a complete aberration due to COVID-19.

The chart above also shows a pretty sharp spike in showings for the rest of April 2021, one-year ago. It will be interesting to see if that trend is matched here in 2022. I suspect that showings will increase as they tend to do in the months of April and May, but the rate of increase will continue to lag that of 2021.

Predictions

It may take a full year or more to get back to stabilized price levels, but I think we may be experiencing peak inflation right now and things will ease a bit in the next 4-6 months, especially if the Fed does start to hike interest rates by 50 basis points at a time. I also think supply chain issues are going to continue to settle out.

You don’t have to just take my word for it, however. UBS, which has made fairly accurate inflation predictions over the past year, is projecting that this Tuesday’s inflation number is going to be a doozy: 8.5%. But they also predict that this will be the peak. The chart below, via Fortune, shows UBS’s assessment of future inflation over the remainder of the year:

One Final Thing

Of course, the inflation story should not be looked at with rose color glasses. Inflation continues to surge in crucial categories like food prices, which hit low and moderate income families the hardest. Those same families are the ones who would be most hurt by an economic recession, however deep or mild it could potentially be. These implications are among the reasons why the skill of the Federal Reserve in managing inflation and the acumen of our political leaders to set reasonable expectations and to respond with effective policies alongside whatever the Fed does will be so crucial over the months to come. Unfortunately I don’t have a lot of confidence in either. Stay tuned.

Ben Sprague lives and works in Bangor, Maine as a V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram.

I spent three days this week in Louisville at a Feeding America conference. I am proud to be the Vice Chair of the Board of Directors for Good Shepherd Food Bank here in Maine. Inflation among food prices is one of the particularly worrisome things to me right now. But I enjoyed the conference in Louisville and learned a lot. It was nice to travel again and to be in the presence of other people in-person rather than via Zoom!