The Low-Hire/Low-Fire Labor Market

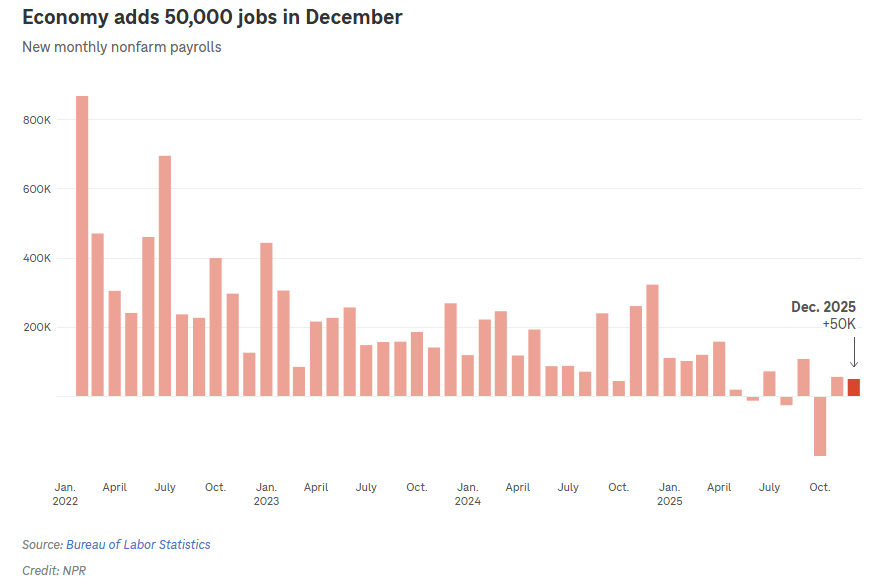

Two weeks ago, I wrote about how AI fears are hitting the consumer, but AI is not the only thing that has people feeling on edge these days as far as the labor market is concerned. Consider the chart below of job growth over the past three years. There is still some fuzziness in the 2025 data and the numbers may change as things continue to be analyzed, but the downward trajectory of new jobs in the economy and the fact that job growth was essentially flat to negative in 2025 are clearly evident:

The past year was not just anemic as compared to recent history, but was actually the worst year for job growth since 2009. There were really only three major sectors that showed job gains in 2025: healthcare, social services including eldercare, and hospitality, which includes travel, hotels, and restaurants.

Other major sectors were down for the year, including manufacturing and warehousing (continuing a multi-year trend). Construction was mostly flat. Federal workers were down notably. In fact, in the chart above, the large decline in the October report was mostly reflective of federal job cuts. There were modest job increases in other areas of government including at the local level, such as police and public works, and in schools and education, but not enough to counteract large job losses at the federal level.

White-collar jobs including office work, banks/finance, and IT/tech were down in 2025, as well, particularly in the latter half of the year. Traditional white-collar jobs represent about 20% of all jobs in the economy and about 40% of GDP, so when there is a pullback here, it can ripple through, for sure.

As economist Heather Long of Navy Federal Credit Union put it recently, “In many ways, 2025 was both a white-collar and a blue-collar jobs recession.” That should have people on alert. A decline in both traditionally blue-collar and white-collar jobs at the same time typically happens at the outset of broader economic drops.

What were the reasons behind the weak job market in 2025? I see three major ones, some of which I have already alluded to above:

DOGE/Federal cuts: the Federal workforce shrank by about 220,000 employees (about 10% of the overall total) in 2025. This represents a mix of buyouts, retirements in positions that were not refilled, true layoffs, and people just getting the heck out of there.

Immigration: it is hard to pinpoint an exact number in terms of the reduction of immigrant workers who have either been deported or detained or who have simply left the workforce over the past year, but Fed economists have noted, “On average, places experiencing the biggest slowdowns in unauthorized immigration saw the biggest slowdowns in employment growth in construction, manufacturing, and other services.” Beyond construction, the impacts have been particularly notable in the agriculture, hospitality, and caregiving industries.

AI/automation. I have written a lot about this lately (and will be doing so again soon), so I’m going to let this one mostly sit for now. Safe to say, millions of jobs are at risk through technological changes and the implementation of AI in the months and years ahead. We started to see this in earnest in the last half of 2025, which, I believe, is the main reason why job growth numbers were so low in the chart above from May onward. Some employers are either already starting to implement AI and cut jobs, or are preparing to do so.

Keeping all of the above in mind, there is also a case to be made for changes from the normal business cycle impacting the job market. Many of the large tech companies and perhaps some other traditional office-type employers overhired during the pandemic in a chase for talent and due to significant industry growth during this time. Some of the layoffs we have seen over the past year may simply be reflective of so-called “right-sizing” of workforces. That being said, right-sizing is also a convenient euphemism that a CEO can use when they want to cut workers for cost savings or because the jobs have become either partially or totally obsolete due to automation and AI, and it seems less cold and calculating.

I do also think higher interest rates over the past 2+ years have limited job growth. It is harder for businesses to grow and less likely that they will invest in themselves when the cost of financing is more significant. This is, of course, one of the reasons why the Fed actually hiked interest rates in 2023-2024, which was to actually slow things down and not allow the economy to overheat.

Low-Hire/Low-Fire

It’s not all bad news in the labor market, however. There are some enigmas, for sure. The unemployment rate of 4.3% is still at a historically healthy level, for example, and the rate is actually down a tick from December and November (if you can trust the data). People who want to work can generally find jobs, even if frustrations abound about mismatches of skills and wages. A lack of available employees is still one of the top frustrations I hear from business owners I work with, and there are plenty of concerns out there about the work ethic and skills of the next generation coming of age (which is, to be fair, a tale as old as time).

Another positive data point is that wages rose by 3.3% last year. That is nothing to write home about in the great scheme of things, but it is notable that wages outpaced inflation, which ran at about 2.7% last year. Workers therefore made slight gains relative to the rising cost of goods and services.

All in all, we are in this very strange moment where the unemployment rate is low, wages are modestly rising, there may be a jobs wipe out coming due to AI, and yet many employers say they still can’t find the workers they need.

You’re (Not) Fired

There have been plenty of anecdotal stories of companies initiating large-scale layoffs over the past year. But more broadly, however, it does not appear that companies are laying people off, en masse, at least at this point. Many companies are not necessarily hiring, but they are also not firing. This has led to what I have recently heard described as a “Low-Hire/Low-Fire” labor market.

Other than in the tech space, which is going to always be quicker to react to significant technological changes, what I am seeing right now is a subdued market for hirings and firings. Everything has basically slowed down. Instead of the normal churn of people retiring, quitting, switching jobs, or being laid off, everyone is just treading water. Hiring is weak, but layoffs are also low (other than in certain high-profile tech examples), and workers are generally staying put. People are trying to hold onto the jobs they have, and fewer workers are moving.

This treading-water mentality includes companies, too, by the way. No one wants to over-hire right now and be left with unnecessary personnel costs. Many employers are also not over-firing, because they also recognize how hard it is to attract and retain good people right now. Many others know that AI and automation are likely to provide massive efficiencies and cost-savings over time, but they don’t necessarily know what that means or how to implement it yet, so they are holding off on reducing their headcounts as there is just still so much that is unknown.

What It All Means

In researching this topic on the labor market this week, I have started to see an odd parallel to the 2020-2024 housing market. One of the major themes during that period of time was that people were essentially staying put. In the housing market, it was a combination of the interest-rate lock-in effect and rapidly rising prices that had people not wanting to give up what they had in order to move into a higher-priced market at notably higher interest rates. The effect was that the market basically froze; prices stayed elevated, but fewer transactions took place, and there was not the usual churn you need in a housing market of people coming and going, upsizing and downsizing, etc., that leads to a healthy rate of new listings and transactions. You need some movement to create opportunities for people, especially those just coming of age into the market.

A similar phenomenon is unfolding today in the labor market. Whereas a few years ago, it seemed like people were switching jobs all the time and constantly trying to move “upmarket” in terms of salary and title, today it feels more like people are increasingly trying to just hold onto the jobs they’ve got.

This is actually bad news for the labor market, particularly certain areas of it. Just as the housing market needs some healthy turnover, so too does the labor market. If people hold off on switching jobs when perhaps they otherwise could have or should have made a move, or if they delay retirement due to their own financial worries or lifestyle anxieties, if effectively “blocks” someone else from stepping into their job. And then if that person remains stuck where they are, it is a sub-optimal situation for them marked by professional frustration and financial stagnation, and also blocks someone a rung down on the ladder from moving into that spot (and so on and so forth).

The situation right now is particularly dire for entry-level workers. Not only did this generation (born roughly 1995-2010) come of age with the pandemic massively impacting their high school, college, and early professional years, but they are now trying to launch careers into perhaps the most challenging job market for entry-level workers in history. People ahead of them are not switching jobs as much and therefore creating opportunities for them, and many others are not retiring, which has down-ripple effects all the way to the entry-level. Layer on top of that a potential white-collar entry-level wipe out due to AI, and you’ve got some real pressures in this part of the labor market, which also means real problems for society. How do people grow and excel in a career if the first rungs on that ladder are not available to them? I don’t know the answer, and I suspect collectively we as society don’t know either. More on this topic to come here in The Sunday Morning Post as we try to figure it out together ourselves.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Thoughts and opinions here do not represent First National Bank.

Hi Ben, my father was born in 1915 and he began his working life after college with getting a job with the civilian conservation core, known as the CCC. He learned how to use heavy equipment and how to manage crews of men of various ages, abilities, and motivations. As you know, the CCC created much of our most admired national parks.

When I look at the decay of so many of our cities and rural towns, particularly here in central Maine, I can’t help but dream of crews of men and women learning how to rebuild structures and improve our community parks. I’d love to see young people learn the skills that are not available anymore such as carving, blacksmithing, and molding. I’d love to see public art again created by the spirit that created the murals in our post offices and parks. Just as art has revived some of our downtowns, perhaps it can also revive our appreciation of human abilities and draw more of us into belonging to community.