What Dutch Tulips Teach Us About 21st Century Investing

Author’s note: Happy Mother’s Day to all the mothers and grandmothers out there. I’m very fortunate to have both a great mom who lives down the street from us and a wonderful wife who is a fantastic mother to our three children. Happy Mother’s Day to them in particular. Today's article is about flowers in honor of all the moms.

A strengthening economy. A public health crisis. Asset prices rising to unheard of heights. Ordinary investors rushing into new investments to avoid missing out. Sound familiar? We might as well be talking about GameStop or Dogecoin in the year 2021, but these are certainly not the only examples of random assets skyrocketing in value seemingly out of the blue. One of the first documented investment bubbles in human history was over 400 years ago. It wasn’t gold or currency or real estate that inflated to incomprehensible levels, though: it was tulip bulbs.

A Brief History of Tulipmania

Tulips originated in Central Asia before making their way to Europe in the 16th century. Beloved for their deep bright colors and exotic appeal, tulips had become a much sought after status symbol among society’s elites particularly in Holland at the outset of the 1600s.

What no one expected in the early 1600s, however, was that by 1637 the price of tulip bulbs would have increased by many orders of magnitude, driven by frenzied buying, wild speculation, and the outright euphoria of the masses. Bulb prices would double seemingly overnight and then double or even triple again several times further. Wealthy investors and ordinary citizens alike bought into the surge, seeking out what they hoped would be sure bet on a rapidly appreciating asset.

In his 1841 book, Extraordinary Popular Delusions and the Madness of Crowds, Scottish journalist Charles Mackay, who dedicated a whole chapter to what he referred to as “Tulipmania,” described the atmosphere at the time by saying, “In 1634, the rage among the Dutch to possess [tulips] was so great that the ordinary industry of the country was neglected, and the population, even to its lowest dregs, embarked in the tulip trade.”

He continued:

At first, as in all these gambling mania, confidence was at its height, and everybody gained…everyone imagined that the passion for tulips would last forever, and that the wealthy from every part of the world would send to Holland, and pay whatever prices were asked for them…Nobles, citizens, farmers, mechanics, seamen, footmen, maidservants, even chimney-sweeps and old clotheswomen, dabbled in tulips. People of all grades converted their property into cash, and invested it in flowers. Houses and lands were offered for sale at ruinously low prices, or assigned in payment of bargains made at the tulip-mart.

In his seminal book on the period, Tulipmania, historian and writer Mike Dash writes:

The interest that many Dutchmen developed in the flower trade owed less to the tulip’s natural beauty than to the dawning realization that money could be made in bulbs…

…In the seventeenth century almost all Dutch artisans worked long hours for low wages. When the day’s work was done and they could finally go home, it was to cramped and sparsely furnished one or two-room houses that were in such short supply the rents were high…to people trapped in an existence such as this, the idea that one could earn a good living by planting bumps and sitting back to watch them grow must have been irresistible.

Why did the Tulip Bubble form?

Several variables contributed to the Dutch tulip bubble, all of which have striking similarities to today. First, the Dutch economy, which had been in a deep recession for much of the 1620s, rebounded. As noted by David Roos, following the recession,

…the Dutch enjoyed a period of unmatched wealth and prosperity. Newly independent from Spain, Dutch merchants grew rich on trade through the Dutch East India Company. With money to spend, art and exotica became fashionable collectors items. That’s how the Dutch became fascinated with rare “broken” tulips, bulbs that produced striped and speckled flowers.

With more people having discretionary income thanks to a strengthening economy that had more money flowing through it, tulips increased in popularity and their prices started to appreciate in value. Tulips and tulip bulbs were now within the means of ordinary citizens to acquire, many of whom now had disposable income for the first time in many years, possibly ever. At the same time, the especially wealthy started paying more and more for the rare breeds of tulips, driving up prices even higher the upper end of the tulip spectrum.

Interestingly enough, much like today there was also a public health crisis at the time, which some commentators have linked to the wild speculation in tulip bulbs. The Bubonic Plague was still prevalent in Europe in the early 17th century. In Tulipmania, Mike Dash notes that between 1633 and 1637, which was the peak of the tulip bubble, possibly upwards of 8,000 Dutch citizens died from the plague, including one in eight people in certain cities, so many so that “there were not graves enough to hold the dead.” Dash hypothesizes that the plague created a shortage of labor, which meant that employers had to pay higher wages to get people to work, thus providing extra income and surplus cash for those who did work. Dash also notes that a “mood of fatalism and desperation” was prevalent that led investors to speculate on tulip bulbs with reckless abandon. This similarities in all of this to the past 12-14 months of pandemic life are notable.

And of course, the key driving force behind the continually appreciating values of tulip bulbs was the dynamic nature of the momentum itself. Then, as now, as the price of an investment increases, people start to buy more of it, hoping to latch onto the upward ride. This buying begets more buying as some people, flush with the euphoria, dopamine, and extra cash from their initial successful investments buy even more, while many of those who have been on the outside end up begrudgingly joining the game to avoid missing out. There becomes a pressure almost born out of jealousy or at least the fear of missing out for people to take part. At such times it can feel like prices will keep rising forever. Mike Dash writes:

Those who tried the bulb trade and profited from it could not resist telling their friends and family about the source of their good fortune; the novelty and implausibility of making money from flowers ensured that their stores were told and retold…by the end of 1634 or the beginning of 1635, lurid tales of the money to be made in tulips were the talk of Holland.

The Bubble Bursts

Absurd anecdotes abound from this time period, some of which may or may not be fully true, perhaps embellished by talented storytellers over the years. There is one story of a sailor who had returned home from a long trip at sea and was unaware of how much tulip bulbs had increased in value during his absence. After spending some time visiting the home of his wealthy friend, the friend leaves the room only to return to find the sailor eating one of his most prized tulip bulbs with a knife and fork.

In Tulipmania, Mike Dash shares numerous anecdotes like this, including a purportedly true story of how a man once sold his house in the town of Hoorne for three tulip bulbs:

When news of the sale of the tulip house got out, a Frisian farmhouse and its adjoining land also changed hands for a parcel of bulbs. These remarkable transactions, which took place in a part of the United Provinces that had been badly battered by a recession, were the first sign that something approaching a mania had been to flourish…now — for the first time — tulips were being used as money. And just as strikingly, they were being valued at huge sums.

Eventually all investment bubbles burst. The collapse of the Tulip Bubble is pinpointed to a specific time and date: the first Tuesday of February 1737. It was on that day that a group of traders met in the Dutch city of Haarlem to buy and sell bulbs. When the auction began, there were no bids on the first set of bulbs. The auctioneer lowered the price, but there were still no bids. He lowered it again, but there were still no bids. Mike Dash illustrates the event by saying, “It is easy to imagine the awkward silence that must have descended upon the group of florists…the half-drunk tankards of beer hanging in midair, partway to the lips of drinkers who suddenly understood the importance of what was happening in front of them.”

The bubble had burst. And it was not even that the bulbs that were to be sold in the coming days were now being sold for just a bit less; it was that the market disappeared entirely. Bulbs could not be sold at all. Mike Dash notes, "In most places the tavern trade crashed so completely that it was not even a question of prices falling to a quarter or tenth of what they had been when the mania was at its peak. The market for tulips ceased to exist.”

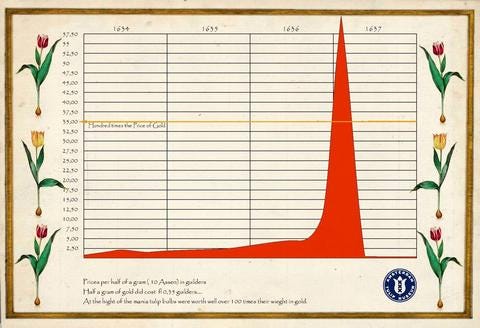

The chart below courtesy of the Amsterdam Tulip Museum, illustrates both the steep rise during the middle of the 1630s and the even more rapid descent at the outset of 1637:

Back to the 21st Century

It would be easy to read the history of Tulipmania and shrug it off as as the misguided dealings of ignorant novices in a distant past. But several of the primary variables that contributed to the Tulip Bubble are as prevalent today as they were then. The worldwide economy including here in the United States has spent the better part of the last decade recovering from the Great Recession, much like the Dutch economy in the 1620s and 1630s. A health crisis has not only added to our collective economic uncertainty, but also has added a sense of fatalism and recklessness to people’s financial dealings. And who among us has not seen a friend or colleague gush on Facebook about their successes trading in investments like GameStop, Dogecoin, and Bitcoin? Who has not been at least curious to see if they, too, can match their friends’ investment success? In fact, a study released in early February 2021 noted that millions upon millions of Americans participated in the so-called meme stock fervor during the month of January:

The stories people have shared in recent months, which are almost entirely about their upside, have increased the feverish tendency of more people to buy in, which, as seen in the Tulip Bubble, only increases prices further. It’s not hard to draw a comparison between Dutchmen and women in the 1630s, who Mike Dash notes lived a cramped and somewhat dull existence, and men and women today who are bored with the drudgery of their own lives especially with COVID-restrictions layered upon all aspects of everyday life for the past year.

The problem for investors during a market bubble is that eventually you run out of buyers. Moreover, markets naturally correct themselves. In February 1637, the tulip market ran out of buyers and prices immediately cratered. But even if the exorbitant prices had lingered on, the market would have corrected itself soon as an increase in supply was also coming. By 1638, tulip producers had proliferated, creating and expanding new growing operations with the hope of capitalizing on the previous high prices. In this particular case, prices had already dropped and there was suddenly an abundance of unneeded supply. But even if high prices had lingered on, this new supply would have at least dampened prices and perhaps acted as a catalyst for a market correction if not a full bursting of the bubble. (As an aside, recent readers of The Sunday Morning Post newsletter will note that this is what I expect to happen with lumber prices over the next 12-24 months as producers expand capacity to take advantage of rising prices; the subsequent increase in supply will ease prices and serve as a catalyst for a reversal of the boom, dare I say bubble, in lumber prices. Click here to read my recent lumber prices newsletter).

Lessons for Today

What are the lessons to take from Tulipmania? Warren Buffet’s age-old investment axiom, “Be fearful when others are greedy, be greedy when others are fearful” comes to mind. If it seems too easy to make money in something and that the market is full of only winners amid continually rising prices, it is probably time to press pause and take a breath. A Facebook post to say, “I’m sitting out GameStop” is not as much fun as posting “Pour everything you’ve got into GameStop!!!” But no one posts about their investment losses on Facebook, either, and GameStop posts on Facebook have become less common since the stock’s dizzying 52-week high of $483/share in January 2021; the stock is currently trading at $161.11/share as of the time of this newsletter.

Time will tell what becomes of 2021’s investment bubbles. In fairness to investors, it can be hard to tell you’re in a bubble until it bursts. But based on the lessons of Tulipmania, bubbles pop, markets correct, and you don’t want to be the last one holding the bag. The charts for numerous investments over the past year including the aforementioned GameStop, Dogecoin, a dozen other viral stocks, and new assets like Bitcoin and other cryptocurrencies not to mention so-called non-fungible tokens (“NFT’s”) are extraordinary. But in their exorbitant heights and the euphoria they have created, they do share many of the characteristics of classic investment bubbles including that brief period of time in the 1630s when Dutch tulips were among the most valuable assets in the entire world.

Ben Sprague lives and works in Bangor, Maine as a V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com. Follow Ben on Twitter, Facebook, or Instagram and subscribe to his weekly newsletter by clicking below.

The Sunday Morning Community

“Thank you to everyone who has been subscribing to the Sunday Morning Post and sharing the articles with your friends and colleagues on social media or by forwarding the emails. I appreciate the messages and feedback I have been receiving from people. In fact, today’s newsletter about Tulipmania was based on several people reaching out after I hyperlinked the single word “tulips” in the lumber article from two weeks ago to say they had never heard of the Tulip Bubble. Thank you all for being a part of the Sunday Morning Post community!” - Ben

A number of people reached out or posted thoughtful comments on Facebook or Twitter about last week’s article about Maine’s labor shortage:

Bob Ziegelaar: “In talking to a wait staff member in Bar Harbor last week I found out she commutes from Bangor on a daily basis because there is no local housing available. Most previously available local space has been absorbed by Air B&B. So workers aren't the only problem. It also points at poor planning at the local level since staff housing has been a longstanding issue.:

Melanie Brooks: “Unless these small businesses or towns have dedicated places for these out of the area workers to live, they can’t come.”

Matthew Haskell: “This could easily be fixed in a very quick manner if they'd increase the yearly H2B cap to 150k workers. End of problem and folks would be amazed at how much better it all works. At how many American jobs those H2b folks create.”

Annie Tselikis: “The temporary foreign worker program, as you note, is critically important for tourism and for seasonal production jobs like lobster wholesale/processing (we use the same H-2B visa and have struggled to get adequate employees for our sector for years). H-2B has been a challenge for the entire seafood industry nationwide - we're in a very similar situation to the tourism industry. It is very frustrating.”

Jack Lutz, PhD, from Forest Research Group based out of Hermon, Maine shared his notes on the rising cost of lumber, listing several factors for why lumber prices have spiked including strong demand from consumers, labor constraints from COVID-19, and labor constraints due to generous unemployment benefits:

Lumber prices have spiked because there is a shortage of lumber and mills have been unable to increase production to meet demand.

US housing starts finished strong in 2020 in spite of a sharp drop in March and April, and home improvement spending remained strong. Sawmill closures resulted in the loss of 2 or 3 (and possibly 4) weeks of production for the year. That drop in lumber production in the face of strong demand led to increasing lumber prices.

Notes:

Talk to your favorite local bookseller about buying Mike Dash’s book, Tulipmania, if you’re interested in learning more about today’s topic. I am indebted to Mike as I relied heavily on his research for today’s newsletter: https://www.penguinrandomhouse.com/books/36938/tulipomania-by-mike-dash/

Tulip Fields The Netherlands today, no longer a bubble but still a prevalent part of the Dutch culture and economy.