Why We Can't Agree on the Economy

In 1983, U.S. Senator Daniel Patrick Moynihan famously said, “Everyone is entitled to their own opinion, but not their own facts.” Why, then, is it actually so hard to agree upon the facts of this current economy, and what does that say about the upcoming election and, just as importantly, the pending election aftermath?

Certain statistics about the economy are unequivocal:

The stock market is at an all-time high. The S&P 500 is up 31% in the last 12 months, and up just over 20% since January. These roaring results have come amid high inflation, consumer pessimism, political turmoil, and global conflict particularly in the Middle East. The market has rolled along through it all.

Inflation is mostly under control. The latest CPI report showed inflation running at a rate of 2.4% year-over-year, which is approaching the Fed’s target rate of 2.0%. Important note, however: of the 2.4% increase, a large portion is based on food and shelter (more on that below).

Employment is stable. The unemployment rate has been around 4.0% for most of the past year, up marginally from the rate of 3.5% from most of 2023, but still hovering near historical lows.

Annualized wage growth has been around 4.0-5.0% for the past year. The strongest gains (by percentage, at least) have come at the lower end of the wage spectrum. Wage growth at all points of the curve is outpacing inflation at this point (although not in all industries; more on that below, too).

The quantitative reality in the facts above should have people feeling buoyant. Yet pessimism and frustration reign supreme. Why?

The Opposite Side of the Economy

One’s views on this economy depend largely on where one sits and, in many cases, the color of the political lens through which one observes it.

The stock market growth is quite positive, but the gains accrue the most to those in the upper wealth categories. According to one statistic, just 62% of Americans are invested in the stock market, which leaves, of course, 38% out of the recent gains. But even further still, 93% of stock market wealth is in the hands of just 10% of the highest net worth investors. Many Americans are only invested in the stock market through their 401(k)’s. While it is nice to see a 20%+ gain on the year, it feels a bit detached from everyday life for people who won’t access those dollars for multiple decades into future.

For many Americans, their lens on the economy is not the stock market at all, but the price of the goods they buy every day. While inflation is easing down, food prices and shelter (i.e. rent and homes) have remained elevated. And since people buy groceries nearly every week, they are constantly reminded of how expensive it is in a way that they might not notice the rising price of, say, air travel or car insurance. And while people can substitute around the things they buy at the grocery store (i.e. boxed pasta instead of more expensive recipes), it’s hard to cut back on groceries altogether.

Shelter is the same way. It’s hard to downsize on rent while rents are increasing everywhere, and no one likes to move every few months. You can get more roommates or move in with family members, but that, too, is not always as easy as it sounds.

The challenges of buying a home especially for new and first-time homebuyers is something I have documented in these articles many times, so I won’t dwell on it here other than to reiterate that the frustrations are so great that many would-be homebuyers have simply given up. What good is a 401(k) that is up 20% for the year if the dream of owning a home feels so out of reach? This has many people feeling hopeless about the economy, and this is a sticky feeling that is not likely to be changed overnight. The parents and grandparents, too, who despair over the younger generation’s inability to access certain core tenants of the American Dream like buying their first home, feel this angst and frustration about the economy even if they themselves are not the ones directly affected.

What about incomes? Isn't there good news there for younger workers? Well, wages have risen the most on a percentage basis for jobs in service and hospitality. Wages have been similarly robust for various professional and white-collar professions. But what is you’re a mill worker? What if you make shoes? What if your plan was to work in your hometown factory after graduating from high school, but then the factory was closed and the job was shipped overseas? What, then, is the good of an unemployment rate around 4.0% if the only jobs that are available are to work at a restaurant, Walmart, or cleaning hotel rooms? This has been what a lot of Americans have been feeling ever since the NAFTA-related factory closures in the 1990s: it creates not just a feeling of hopelessness, but of bitterness too.

Other Factors at Play

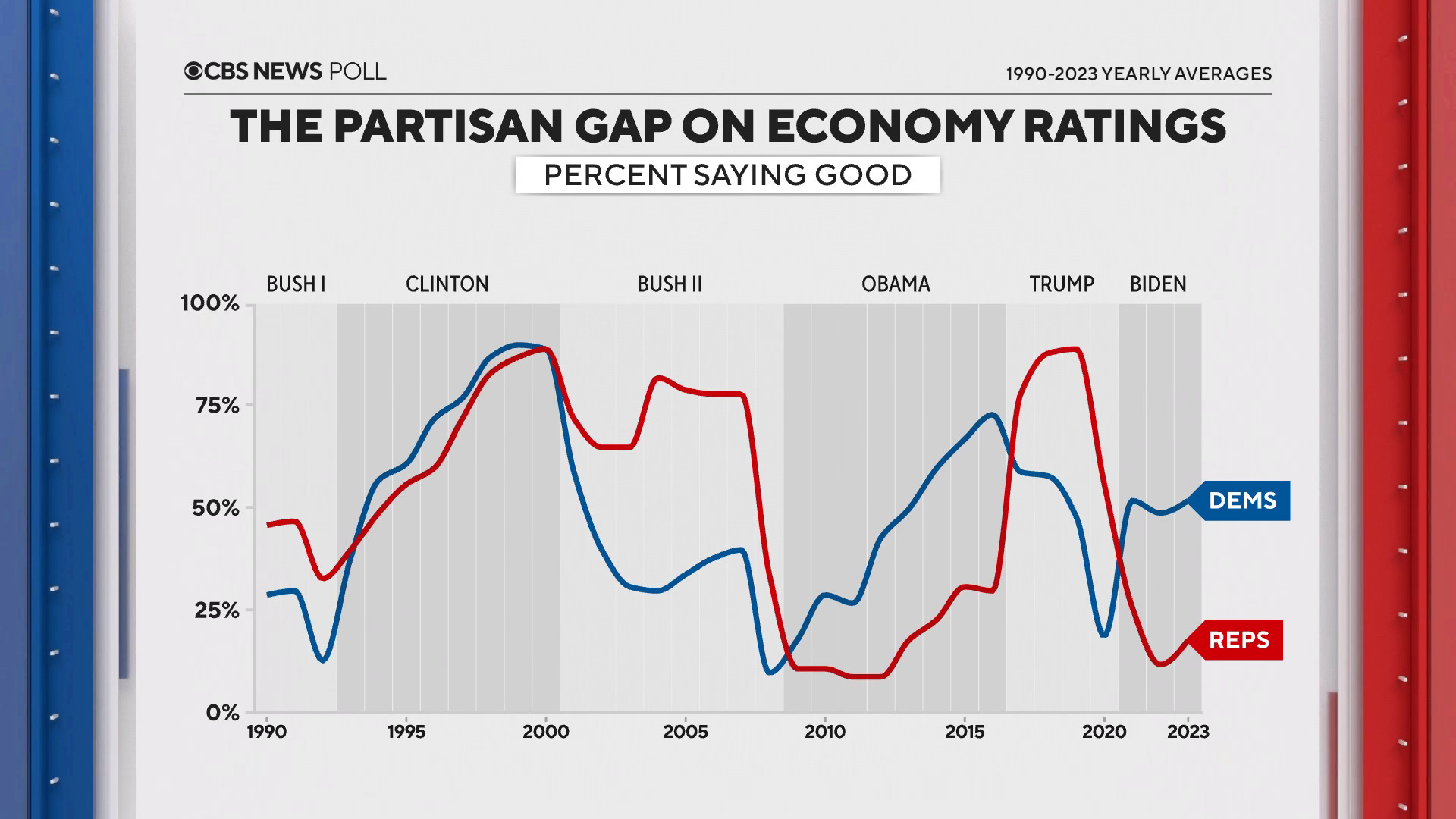

I plan to come back to some of these topics at a later time, but there are a couple of other things at play that lead to people feeling down about what are some otherwise positive economic numbers. The first is, of course, the drug of partisanship. I have shared the chart below previously, but it is worth looking at again, especially on the cusp of a very important election. The chart shows the difference in views on the economy between Democrats and Republicans based on who is in office. In every single presidency in the past 30+ years, Americans of the political party of the president rate the economy more highly than those of the out-party:

Today, there are many Republicans who simply cannot believe that the economy is in good shape under a Democratic president, and vice versa, when a Republican is the president, many Democrats cannot accept that the economy is doing well then. If Trump wins, you can bet in 2025, a majority of Republicans will say the economy is strong while economic sentiment among Democrats will plunge. The opposite will be true if Harris wins.

Lastly, on questions like inflation, for example, people aren’t just reacting to today’s prices, they’re reacting to the rollercoaster of the last few years. The pandemic upended our lives and introduced an unusual era of rapid, often unpredictable economic shifts. People were forced into new work-from-home routines, made sudden career shifts, and experienced supply chain disruptions that affected everything from toilet paper to car parts. That kind of upheaval leaves a mark. Even as conditions stabilize, there’s a sense of uncertainty that lingers. Big-picture, it’s hard to shake the feeling that we might be one disruption away from another economic spiral even if some of the quantitative metrics I shared at the outset of today’s article suggest stability.

What Comes Next

The country could be in for a rough few weeks. According to one recent poll by Pew Research, 40% of Trump supporters are skeptical that the election results will be valid. With the margin on Tuesday likely to be razor thin, there is a real chance that wide swaths of the nation don’t see the results as legitimate. One reason for this is that one particular candidate (Trump) is still telling people the results in 2020 were illegitimate, contrary to any evidence, and he and his supporters have continuously fanned the flames of doubt about the integrity and ability of our institutions to run a free, fair, and accurate election. That will make it very hard if Harris does, indeed, win, which if she does it will likely be by a very narrow margin. A huge portion of the country appears poised to not accept that result.

(Quick aside: the bubbles we live in, which are reinforced by social media algorithms and self-selected news sources, are a huge issue at play here. This is such an important yet broad topic that I plan to come back to it for its own article in future weeks as it deserves its own space).

The Daniel Patrick Moynihan quote at the outset about opinions and facts seems almost quaint today, especially on the eve of such a key moment as the selection of a new president. There is subjectivity in facts, though, as perceptions are based on where one sits, but the interpretation of said facts is also highly affected by the various influences in our lives. More on that to come, and may we all make it through the upcoming week and may our country emerge as intact as possible over the coming days, weeks, and months.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com.