1946 vs. 2026

A look at income tax rates and what it all means

Author’s note: I’ve written two time-comparison pieces previously for The Sunday Morning Post, and today’s article is a third. The first one compared the housing market in 2021 with that of 2007. I wrote it in response to people predicting a popping of a housing bubble (note: it did not happen). The second compared the challenges of buying a home in 2023 with 1983, or, in other words, who had it worse - Boomers or Millennials/Gen Z? You can still read those non-paywalled articles here:

This week we are back with another comparison piece, this one with 80 years of separation.

1946 vs. 2026

“Well our fathers fought the Second World War, spent their weekends at the Jersey Shore.”

-Billy Joel, “Allentown”

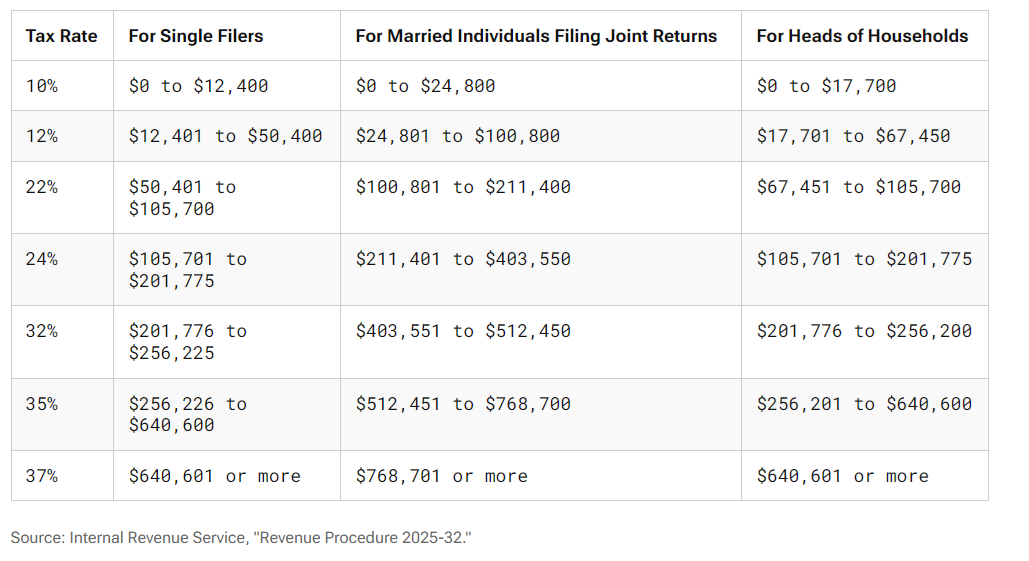

On Thursday, the IRS released its expected tax brackets for 2026. The marginal tax rates are staying the same, but the income thresholds are being modestly adjusted to account for inflation. For example, for single filers, the 24% tax bracket starts at $103,351 of income in 2025, and it will start at $105,701 in 2026. Here is what the full table is slated to look like:

No one likes to pay more than their fair share of taxes, and Americans typically feel chronically overtaxed. Taxation may not feel like the most sexy topic out there, but questions of who should pay and how much they should pay are a standard aspect of modern American political life and, indeed, they always have been since the Sons of Liberty protested the Stamp Act of 1765 (“No taxation without representation!”).

We are not going back to 1765 today (although that would be fun), but we are going to dig into the question of how today’s tax rates compare with those of the past. Grab your Bing Crosby records and a nickel for a glass bottle of Coke, we’re going back to 1946.

A Brief History of the U.S. Income Tax

The history of the income tax in the United States is full of surprises. For starters, the Founders envisioned no such thing. There was no income tax in 1765, nor was there in 1776, nor when the Constitution was signed in 1787. In those early days, the government was funded primarily through tariffs on foreign goods and excise taxes on items like tobacco, whiskey, and many other products. The growing nation also generated revenue from land sales as Americans spread into rural areas and then started moving west.

The first tax on incomes akin to what we would recognize today happened during the early days of the Civil War, when Congress passed the Revenue Act of 1861 to raise funds for the Union war effort. The tax was temporary, and income taxes were abolished altogether by the Supreme Court as being unconstitutional in 1895.

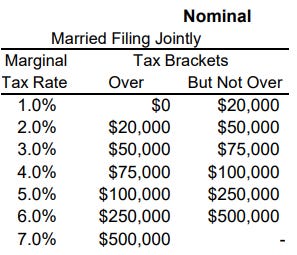

Reformers then pushed for a constitutional amendment that would give Congress the power to tax incomes, and in 1913, the Sixteenth Amendment was ratified, which did just that. Congress subsequently enacted a modest income tax, which at the time, started at 1% and topped out at 7%. Here is what the actual federal income tax brackets looked like in 1913:

By point of reference, an income of $20,000 in 1913 would be about $650,000 today. So the vast majority of incomes back in 1913 were taxed at the lowest marginal rate of just 1%. Not bad, right? The top tax bracket of 7.0% kicked in at an income of $500,000, which would be over $16 million today.

Over the ensuing decades, the income tax evolved from a niche levy into the federal government’s primary source of revenue. World War I and World War II brought major expansions in both rates and reach, as mass taxation became necessary to finance the war efforts. Withholding from paychecks began in 1943, embedding the income tax in everyday life. Since then, the system has gone through waves of reform, but it remains the backbone of federal finance and a defining feature of the modern American economic life.

Peak Tax Brackets

The tax bracket range of 1.0-7.0% lasted through 1915, and the things got interesting. By the end of the decade, the top tax bracket was 73% on incomes over $1,000,000 (not a typo — actually 73%!). There was also a 72% tax bracket on incomes from $500,000-$1,000,000. Tax brackets were higher in order to, among other things, pay for the U.S. war effort in World War I. Brackets then moderated to a range of 1.5-25% for much of the 1920s before the high end started to take off again in the 1930s and 1940s.

The nation was at war again in the 1940s. In 1944, the lowest tax bracket was 23% on incomes from $0-$2,000 ($2,000 is equivalent to about $37,000 today). The top end of the tax bracket was a marginal rate of 94% (!!!) on income over $200,000 (about $3.7 million today). In fact, all income over $50,000 in 1944 (about $920,000 today) was taxed at 78%, and all income over $100,000 (about $1.8 million today) was taxed at 92%!

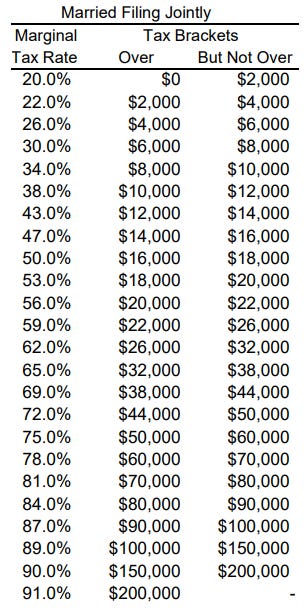

These tax rates generally carried through to the year we are comparing against, 1946, when brackets ranged from 20% on incomes from $0-$2,000 to 91% on incomes over $200,000. Here is the 1946 set of marginal tax rates:

I don’t think most Americans realize how significant the tax burdens were as recently as 1946. Imagine if a mainstream American politician today proposed a high-end tax bracket of 91%. Even though that would only impact about 0.01% of U.S. income earners, anyone proposing a tax structure like that would be branded a socialist, anti-American heretic.

Here is what the tax burden is likely to look like in 2026 for an upper middle-tier American earning $100,000 per year. First, there is a standard deduction of $16,100, so that income is not taxed at all. Bands of income are then taxed at 10%, 12%, and 22%, which totals up to about $13,000 of income tax for someone making $100,000, or about 13% (remember: if your income places you in the 22% tax bracket, not all of your income is taxed at that rate; the first $12,400 of income for you, me, the president, your child’s schoolteacher, Warren Buffett, Warren Buffett’s assistant, and every other income-earning American is taxed at 10%, and so on and so forth).

Looking backward, $100,000 today would be equal to about $6,000 in 1946. I’ll save you all the math, but the taxable impact on that taxpayer in 1946 would have been about $1,450, which is an effective tax rate of about 24%, which is nearly double the tax impact as compared to today. Americans generally were taxed much more in 1946 than they are today, at least from an income tax standpoint (it’s fair to say that property taxes, sales taxes, and other forms of local excise and use taxes are generally higher today as compared to 1946, however).

Final Thoughts

It’s fair to have different views on what the optimal tax rates are at different levels of income. Discussing them is a worthy civic exercise, but beyond the scope of this week’s article. Nonetheless, in many surveys, Americans typically rank the 1950s as the era they would most like to return to (this is generally followed by the 1960s and the 1980s). Very few people tend to rate the 2000s or 2010s as the best era (I can’t imagine people will say the 2020s will have been the best either, but we’ll see).

A key aspect of our collective memory of the 1950s, however, (even for those of us who weren’t alive back then) is the notion that people could own a home, a car, raise a family, and have a little bit extra for savings or to take their family to the Jersey Shore (or wherever). Those things all feel increasingly out of reach for many Americans today, especially those just getting started out.

It’s natural to view nostalgic periods of American live through rose-colored glasses. The 1950s were idyllic for many, and the “Leave it to Beaver” view of American suburbia looms large in the collective memory of the country. For many others, the 1950s weren’t so great (also beyond the scope of today’s article). Few likely remember (or care) that the top-end marginal tax rates stayed in the 91-93% range all the way through the 1950s until 1963, at which point they started to come down. I think it’s fair to ask if those tax rates on high income earners were not just an aspect of American life at the time, but actually a key feature that led to the growing prosperity of America’s increasingly prominent middle class at the time.

The Sunday Morning Post is always free, never pay-walled, and contains no ads. To learn how you can support this work and keep these articles free from clutter, become a paid supporter here or click to read more here.

Ben Sprague lives and works in Bangor, Maine as a Senior V.P./Commercial Lending Officer for Damariscotta-based First National Bank. He previously worked as an investment advisor and graduated from Harvard University in 2006. Ben can be reached at ben.sprague@thefirst.com or bsprague1@gmail.com.

In those days there were tons of expenses that were deductible and all of us took advantage of them to lower our taxes.